Banks Are Quietly Bringing Back These 6 Fees — We Calculated What They Cost You Per Year

In May 2025, Congress quietly killed the rule that would have saved you $225 a year. Most people had no idea it existed — and now the fees are coming back faster than they left.

TL;DR

- Congress repealed the CFPB's $5 overdraft fee cap in May 2025 (P.L. 119-10). Banks can now charge whatever they want again.

- 14 of the 20 largest U.S. banks are already reporting increased overdraft fee income in 2025.

- A typical Chase customer who overdrafts three times a month now pays $1,580/year in avoidable fees.

- The average overdraft fee (Bankrate, 2025): $26.77 — but Chase charges $34 and Wells Fargo charges $35.

- Online banks charge $0 for the same behavior. Switching takes about 15 minutes.

Table of Contents

- The Regulation That Was Supposed to Save You $225/Year

- The 6 Fees Making a Comeback

- We Did the Math: Three Scenarios

- Who Actually Pays These Fees?

- What to Use Instead: Overdraft Protection Options

- Frequently Asked Questions

The Regulation That Was Supposed to Save You $225/Year

In January 2025, the Consumer Financial Protection Bureau finalized a rule capping overdraft fees at $5 per transaction. According to the CFPB's own estimates, that rule would have saved American consumers $5 billion per year — roughly $225 per household.

Congress repealed it in May 2025 via the Congressional Review Act (P.L. 119-10). Under the CRA, the CFPB cannot issue a substantially similar rule without new legislation. This isn't a temporary policy setback — it would require an act of Congress to undo.

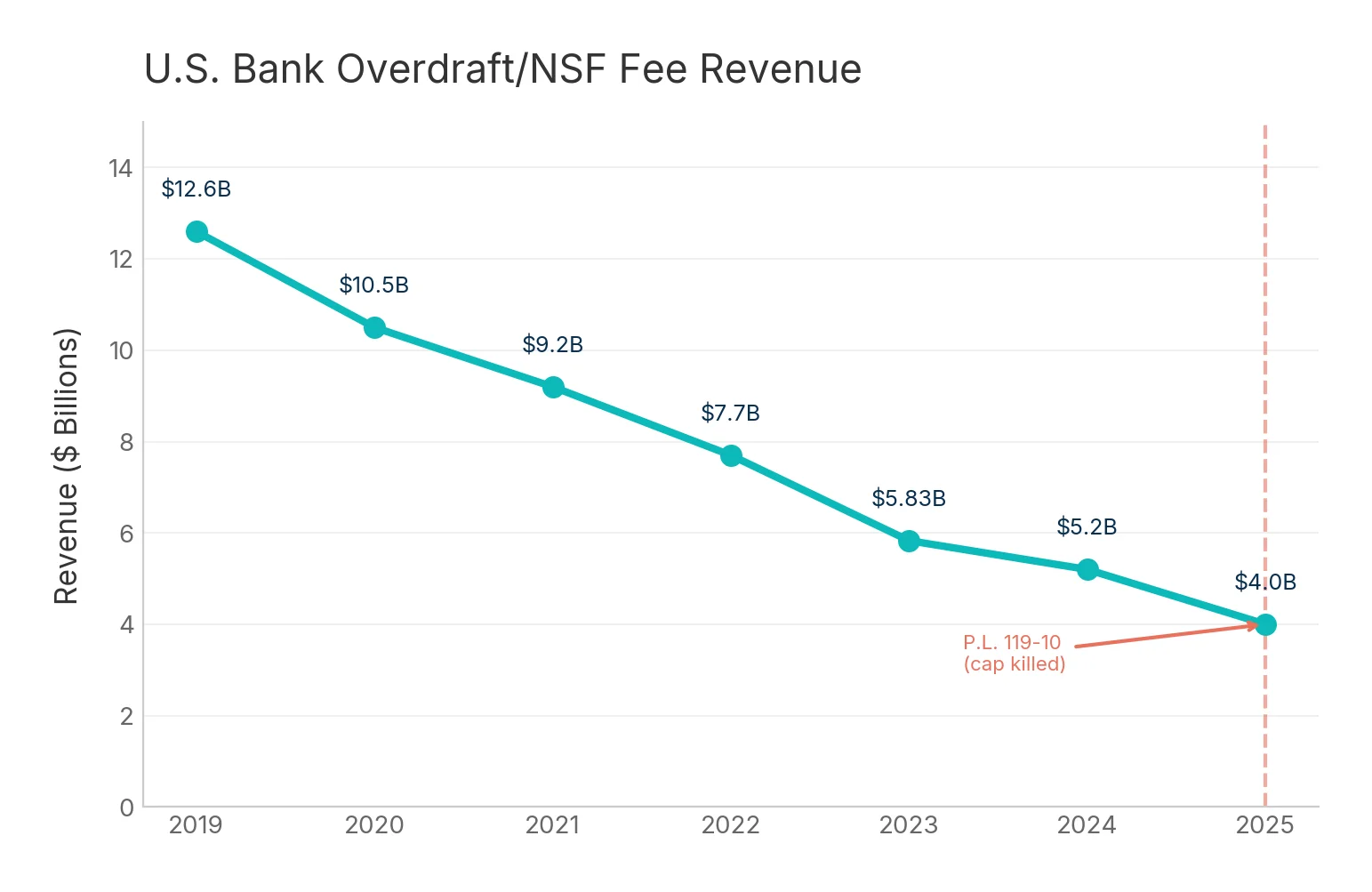

The result was predictable. Reuters and FFIEC data show the top 20 U.S. banks collected $2.99 billion in overdraft and NSF fees in just the first three quarters of 2025 — a 2% year-over-year increase after four consecutive years of declining fee income. More telling: 14 of those 20 banks reversed course and are now growing this revenue line.

The fee reversal didn't start with overdrafts. Banks had already spent 2021–2024 quietly raising maintenance fees and tightening balance requirements to offset lost overdraft revenue during the reform era. Per SavingAdvice.com (March 2026), banks explicitly cited "lost overdraft revenue" as justification for maintenance fee hikes. Now consumers are being double-billed: the overdraft fees are back and the maintenance fees that were raised to replace them haven't come down.

These aren't the only recurring charges quietly draining accounts. Our subscription audit found Americans average $219/month in subscription costs while thinking they pay $86. Stack the $133/month subscription gap on top of $1,580/year in bank fees and you're looking at $3,180+ a year evaporating before you even buy groceries.

The 6 Fees Making a Comeback

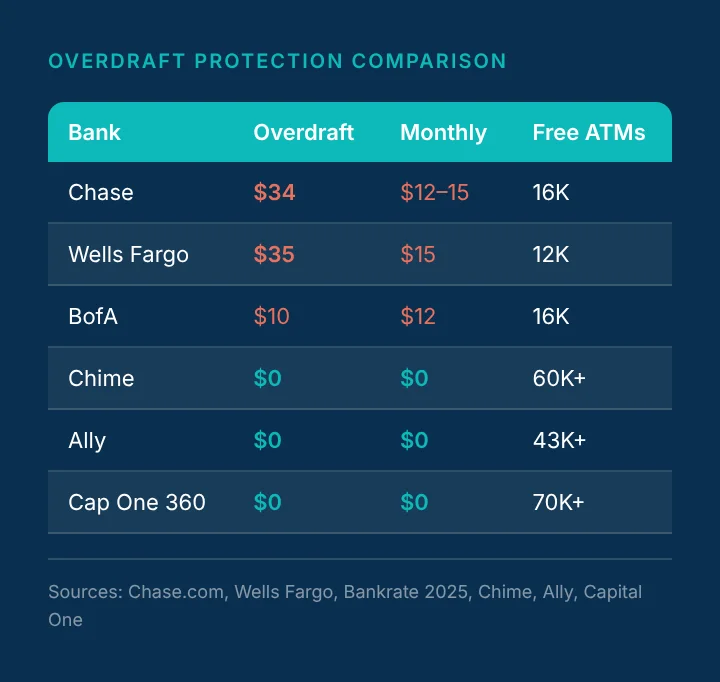

1. Overdraft Fees

The headline fee. 94% of bank accounts still charge overdraft fees, according to Bankrate's September 2025 survey. The industry average is $26.77 per transaction — but that number is pulled downward by Bank of America's $10 outlier. If you bank at Chase or Wells Fargo, you're paying $34–$35 per overdraft, with Chase capping daily charges at $102 (three overdrafts/day).

2. Non-Sufficient Funds (NSF) Fees

When a transaction is declined instead of covered, many banks charge an NSF fee rather than an overdraft fee. These are sometimes charged even when you don't go negative — the transaction doesn't process, but you're still penalized $25–$35 for attempting it.

3. Monthly Maintenance Fees

The average monthly maintenance fee is now $13.95/month ($167.40/year), according to MoneyRates (January 2026). Large banks average $16.35/month. Wells Fargo raised its monthly fee from $10 to $15 in October 2025 — a 50% increase — while simultaneously tripling the minimum daily balance required to waive it from $500 to $1,500. Both moves came in the months after the CFPB rule was killed.

4. Out-of-Network ATM Fees

A single out-of-network ATM withdrawal now costs an average of $4.86 total — your bank's fee plus the ATM operator's fee. That's a record high for the third consecutive year, per Bankrate's 2025 checking account survey. As ATM usage declines, banks charge more per transaction to protect revenue.

5. Paper Statement Fees

Bank of America, Wells Fargo, and Fifth Third have all implemented $5/month paper statement fees (Business Insider, April 2025). Opting into paperless banking eliminates this one — but it requires you to notice it exists.

6. Minimum Balance Penalties

Below a minimum? You pay. The threshold is moving upward. Wells Fargo's balance-waiver threshold jumped from $500 to $1,500 in 2025. That's a meaningful difference: households with median checking balances of a few hundred dollars can't avoid the fee regardless of behavior.

We Did the Math: Three Scenarios

These aren't worst-case estimates. They're based on published fee schedules from Chase, Wells Fargo, and Bankrate's verified 2025 data.

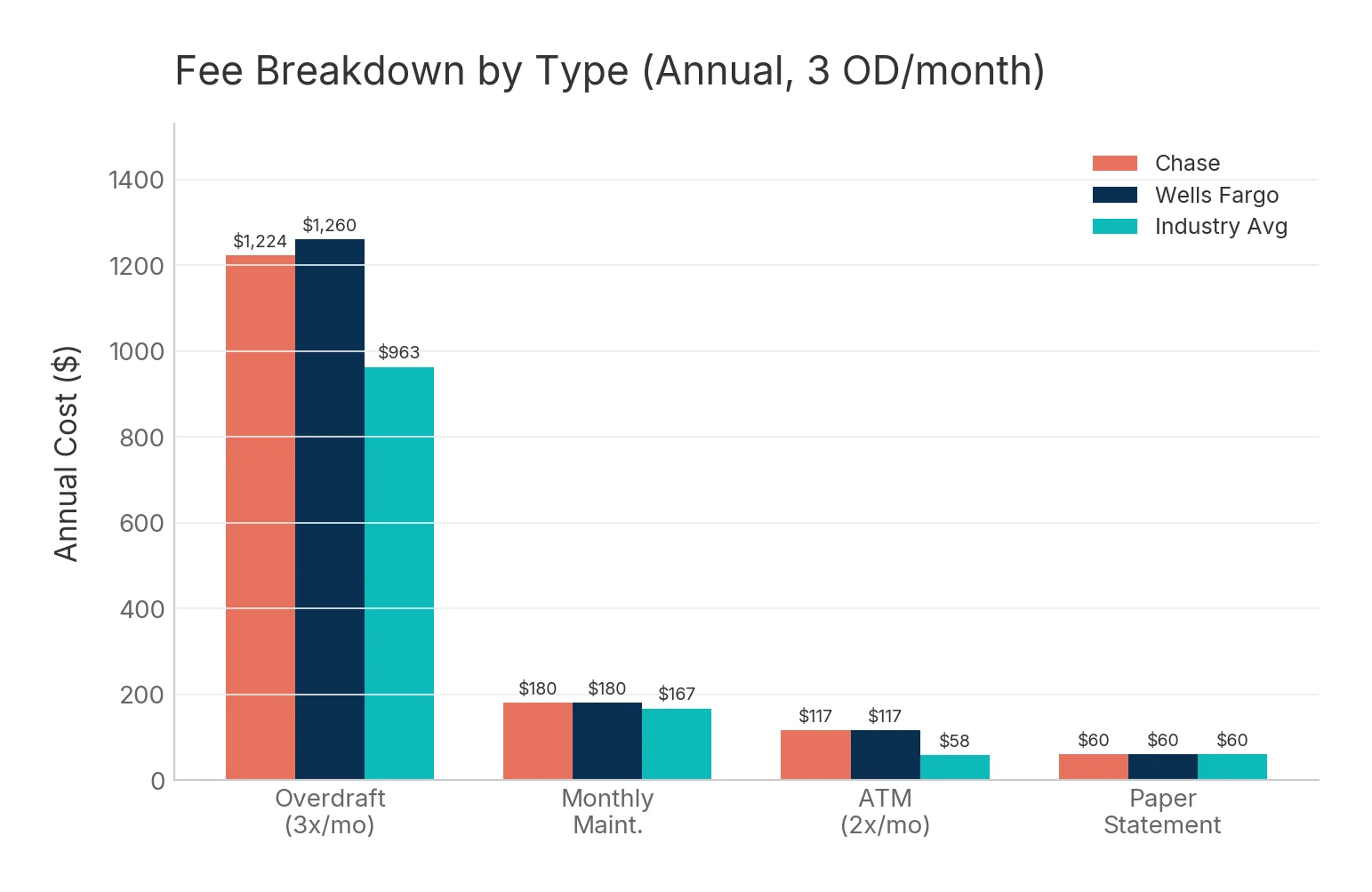

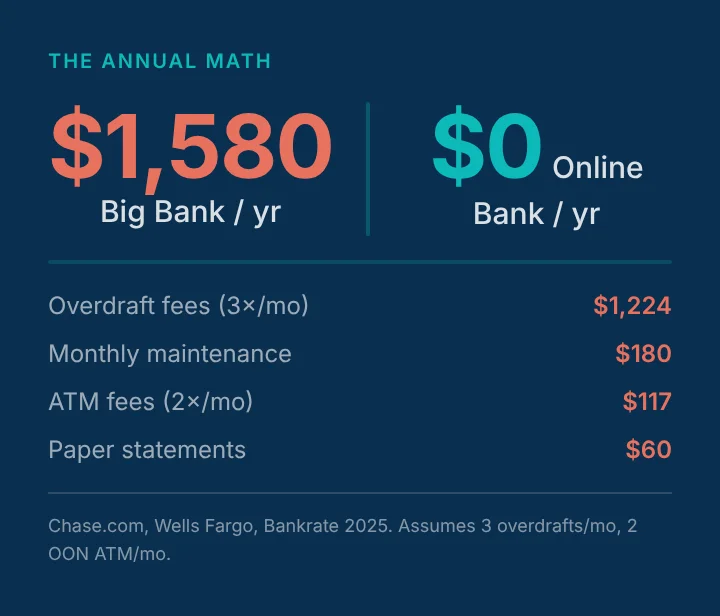

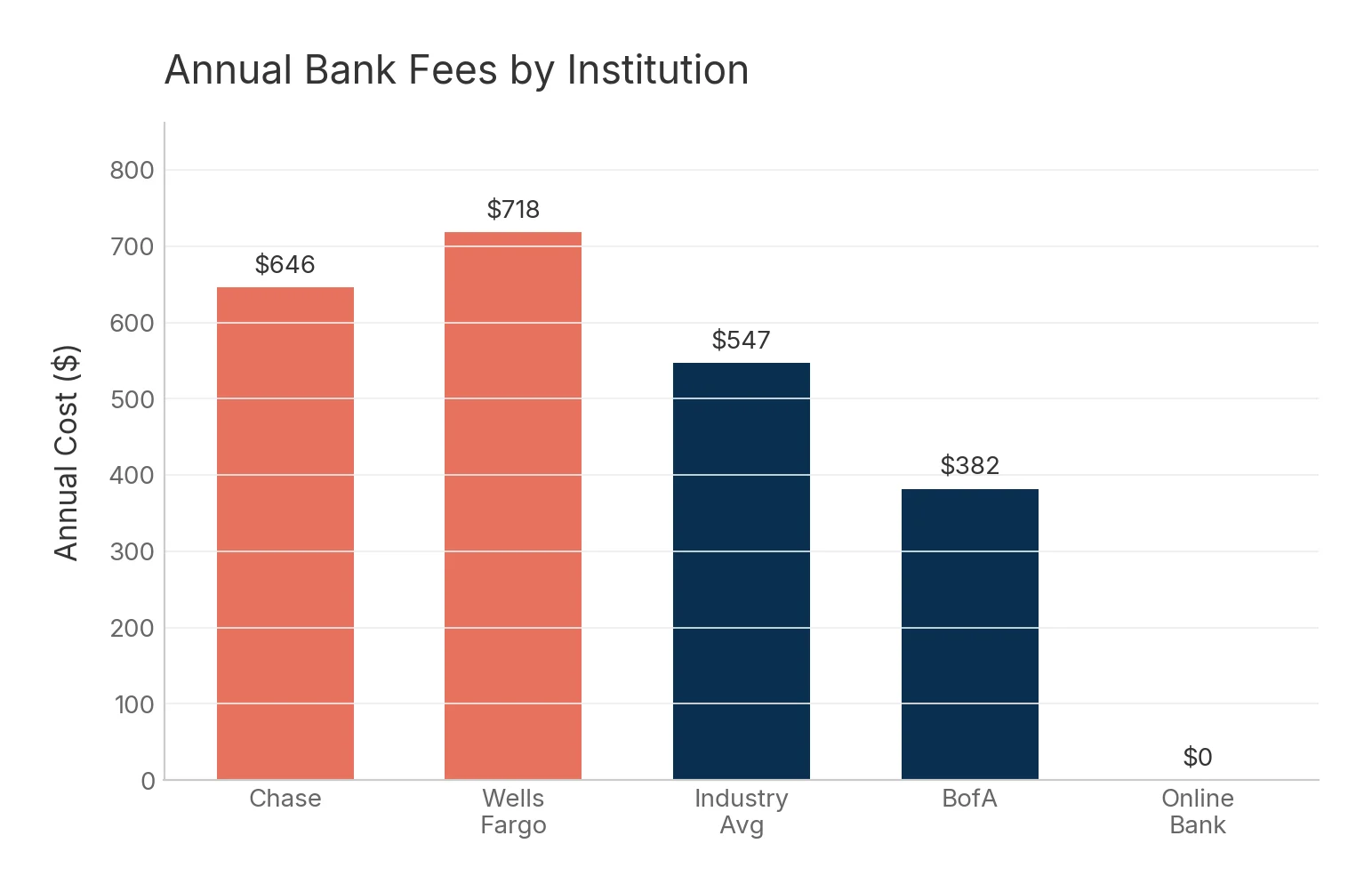

Scenario A: Typical Affected Customer (3 overdrafts/month, Chase)

| Fee | Calculation | Annual Cost |

|---|---|---|

| Overdraft fees | 3 × $34 × 12 months | $1,224 |

| Monthly maintenance | $15/month (Wells Fargo new rate) | $180 |

| Out-of-network ATM | 2 × $4.86 × 12 months | $117 |

| Paper statement fee | $5/month × 12 months | $60 |

| Total | $1,581/year |

Scenario B: Moderate Consumer (CFPB average behavior)

| Fee | Calculation | Annual Cost |

|---|---|---|

| Overdraft fees | CFPB average for households that overdraft | $185 |

| Monthly maintenance | $13.95/month industry average | $167 |

| Out-of-network ATM | 1 × $4.86 × 12 months | $58 |

| Paper statement fee | $5/month × 12 months | $60 |

| Total | ~$470/year |

Scenario C: Online Bank (Same Behavior, Zero Fees)

| Fee | Annual Cost |

|---|---|

| Overdraft (Chime SpotMe) | $0 |

| Monthly maintenance | $0 |

| ATM (60K fee-free network) | $0 |

| Paper statement | $0 |

| Total | $0/year |

The difference between Scenario A and Scenario C isn't behavior — it's the institution. The same financial habits that cost $1,581/year at a big bank cost nothing at an online bank.

Who Actually Pays These Fees?

The fee burden isn't evenly distributed.

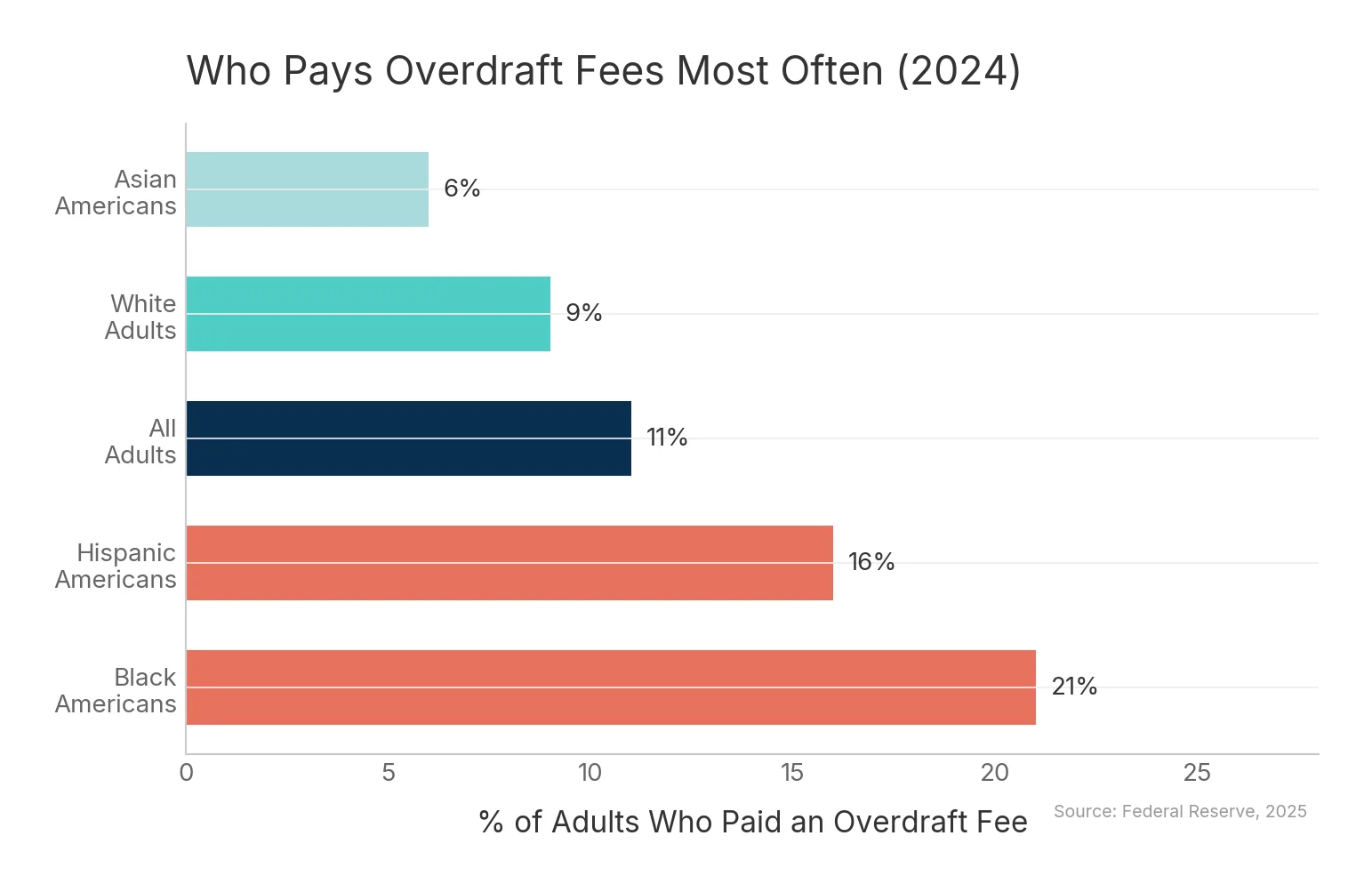

The Federal Reserve's 2025 Economic Well-Being of Households report found that 11% of U.S. adults paid an overdraft fee in 2024 — but that figure jumps to 21% for Black Americans and 16% for Hispanic adults, compared to 9% for white adults.

The CFPB's own data (confirmed by the National Consumer Law Center in 2025) shows that the overdraft fee burden is extraordinarily concentrated: just 9% of accounts pay 79% of all overdraft fees. These frequent overdrafters (10 or more per year) tend to have low account balances — often only a few hundred dollars — and pay an estimated $380/year in overdraft fees alone.

The financial logic is grim. High fees drain low balances. Drained balances trigger more overdrafts. More overdrafts trigger more fees. Eventually the account closes. The customer becomes unbanked — and the cycle repeats.

And this is all happening while non-bank costs squeeze the same households: the recent jump in gas prices increase weekly cost by $47/week for the average driver, which is exactly the kind of shock that produces the overdraft in the first place. The fee isn't a consequence of "bad money habits" — it's a consequence of thin margins meeting rising prices.

What to Use Instead: Overdraft Protection Options

If you're searching for an overdraft protection app, you're already ahead of the 23 million households paying $34 a hit. Here's what actually works.

No-Fee Online Banks

These institutions don't charge overdraft fees as a product design decision — not as a waivable feature. We verified every number from the banks' own fee disclosures in our full overdraft protection app comparison.

- Chime: SpotMe covers overdrafts up to $200 with no fee, no interest. Zero monthly maintenance. 60,000 fee-free ATMs.

- Ally Bank: $0 overdraft fees, $0 monthly fee, and up to $10/month in ATM fee reimbursements.

- Capital One 360 Checking: $0 overdraft fees, $0 monthly fee, 70,000 fee-free ATMs.

Cash Flow Support Apps

For the moments when your checking account runs thin before your next deposit — not just when you accidentally go negative — cash flow apps can bridge the gap.

Panda Pay gives eligible users up to $100 in temporary cash flow support through Cash Flex™ — with no interest, no late fees, and no credit check. It's a tool for managing the timing gaps that make overdrafts happen in the first place.

Call Your Bank First

If you've had an overdraft fee in the last 12 months and you've been a customer for more than a year, it's worth calling and asking for a one-time waiver. Many banks grant these routinely for long-standing customers.

Frequently Asked Questions

What is the average overdraft fee in 2025?

The national average overdraft fee is $26.77 across all banks, according to Bankrate's September 2025 checking account survey. That figure includes Bank of America's $10 outlier, which skews the average down. If you bank at Chase or Wells Fargo, you pay $34–$35 per transaction.

Why are bank fees going up in 2025?

Congress killed the CFPB's $5 overdraft fee cap via the Congressional Review Act (P.L. 119-10, May 2025). Under the CRA, the CFPB cannot reinstate a substantially similar rule without new Congressional authorization. Banks also raised monthly maintenance fees during the 2021–2024 reform era to offset lost overdraft revenue — and those increases are staying in place even as overdraft fees return.

What is the best overdraft protection app?

The most cost-effective options are online banks that charge no overdraft fees by design — Chime (SpotMe up to $200, $0/month), Ally ($0 overdraft fees, $0/month), and Capital One 360 ($0 overdraft fees, 70K free ATMs). For managing cash flow timing gaps before a transaction fails, apps like Panda Pay offer eligible users up to $100 in temporary support with no interest or late fees.

Can I get my overdraft fees waived?

Yes — call your bank and ask. Most banks will waive one overdraft fee per year for long-standing customers, especially if the overdraft was small and quickly resolved. The phrase "I'd like to request a one-time courtesy waiver" is well-understood by bank customer service reps.

How much do Americans pay in overdraft fees each year?

The top 20 U.S. banks collected $2.99 billion in overdraft and NSF fees in the first three quarters of 2025 alone. Full-year 2023 totals hit $5.83 billion. Since 2000, Americans have paid an estimated $280 billion in overdraft fees — a figure documented by the CFPB and reported by CNBC in December 2024.

Conclusion

The math isn't complicated: a $34 fee on a $15 overdraft, three times a month, at a bank that raised its maintenance fee by 50% last fall. The regulatory window that might have capped those fees is closed — and under current law, it won't reopen without an act of Congress.

The good news is that a $0 alternative has existed for years. Chime, Ally, Capital One 360, and others have built $0-fee checking accounts on the premise that overdraft fees shouldn't exist. If you're paying them, you're subsidizing a revenue model you don't have to. Our guide to zero-overdraft banks breaks down which accounts are actually free and how to switch in about 30 minutes.

These fees are one piece of a larger pattern. Our analysis of the cost of being broke in America in 2026 calculates the full poverty penalty — bank fees, insurance surcharges, payday loans, and regressive tariffs — at roughly $3,023 a year for a $35,000 household.

And for the moments when timing is the real problem — when rent is Thursday and payday is Friday — Panda Pay gives eligible users up to $100 in temporary cash flow support through Cash Flex™. No interest, no late fees, no credit check. Just a little breathing room.

$280 billion since 2000. You've already paid enough.