The Paycheck-to-Paycheck Penalty: What It Actually Costs to Be Broke in America in 2026

Living paycheck to paycheck costs more than you think. Being broke isn't just about having less money — it's about paying more for everything.

We spent weeks pulling fee disclosures from 20 US banks, cross-tabbing Federal Reserve survey data with BLS spending data, running Yale Budget Lab tariff models, and computing what a $35,000/year household living paycheck to paycheck actually pays in hidden penalties — overdraft fees, subprime interest, insurance surcharges, regressive tariffs, and more. The total: $3,023/year in universal costs alone. That's $252 every month. $8.28 every day. Gone — not because you spent it, but because the system charges you more when you have less.

TL;DR

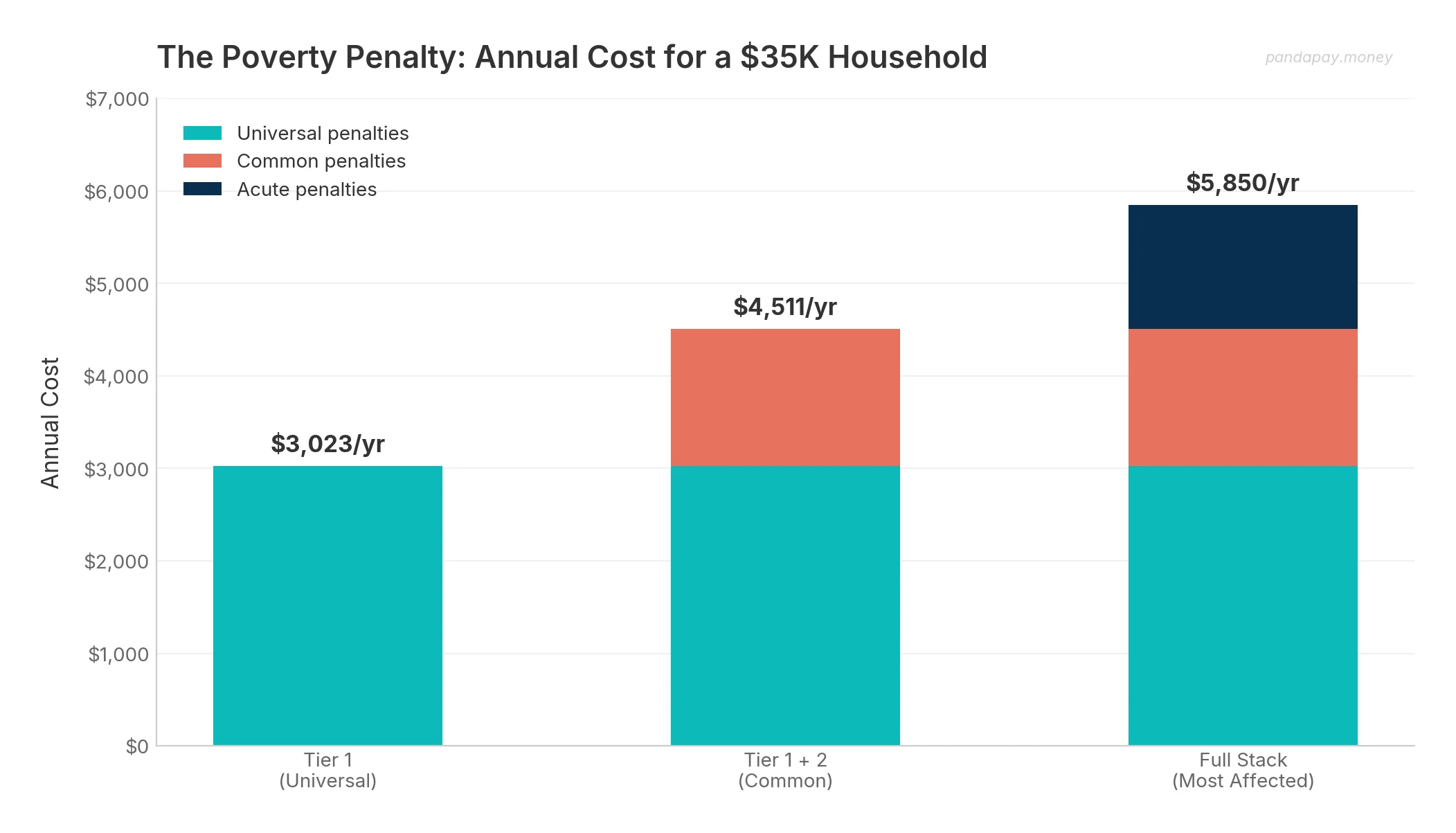

- The poverty penalty costs a $35K household $3,023/year in unavoidable hidden costs — and up to $5,850 for the most affected

- The single biggest component: subprime auto loan interest ($1,134/year) — same car, different credit score, $5,668 more over the loan

- Auto insurance adds $749/year just for having poor credit — even with a clean driving record

- Overdraft fees are declining (down 51% since 2019) but Chase, Wells Fargo, and US Bank still charge $34-36 per transaction

- The penalty is deeply regressive: 8.6% of a $35K income vs 0.2% of a $100K income

- Three moves can cut $2,000+/year from your penalty — we break them down at the bottom

Data & Methods

For this post, we scraped fee disclosures from 20 US banks on April 11, 2026, and cross-tabbed the results with Federal Reserve SHED 2024 survey data, BLS Consumer Expenditure Survey 2024 income-quintile data, Yale Budget Lab tariff distributional models, CFPB overdraft data, and insurance industry rate analyses. Every dollar figure is sourced, calculated, and auditable — see the Methodology Appendix at the bottom.

Table of Contents

- Why Does Living Paycheck to Paycheck Cost So Much? — The concept, why it exists, and who it hits hardest

- The 10 Components (With Math) — Every penalty, every dollar, every source

- Bank-by-Bank Overdraft Fees — Our dataset from 20 banks, updated April 2026

- $35K vs $75K: Side by Side — Same expenses, different costs

- The Counter-Arguments — We address the strongest objections

- How Can You Stop Living Paycheck to Paycheck? — Three actionable moves, starting today

- FAQ — Quick answers to the most common questions

- Methodology Appendix — Full audit trail for every calculated figure

Why Does Living Paycheck to Paycheck Cost So Much?

The poverty penalty is the structural surcharge on having less money. Lower-income people pay more for the same car loans, the same insurance, the same checking accounts, and the same groceries — not because they're making bad choices, but because the pricing systems are built that way.

Credit-based insurance scoring charges you more for car and renters insurance because your credit score is low. Subprime auto lending charges you triple the interest rate. Banks charge monthly fees you can't waive because you don't have enough in the account. Tariffs hit your grocery bill 3x harder as a share of your income than they hit a wealthy household's.

According to the Federal Reserve's 2024 SHED survey, 37% of American adults still can't cover a $400 emergency expense with cash. According to Bank of America's 2025 analysis, 24% of all households spend 95% or more of their income on necessities. And with only 28% of workers saying it's a good time to find a new job, switching to higher-paying work isn't the escape valve it used to be. These aren't people making bad decisions — they're people being charged extra for existing in a system designed for people with more cushion.

We wanted to know exactly how much that surcharge costs. So we calculated it.

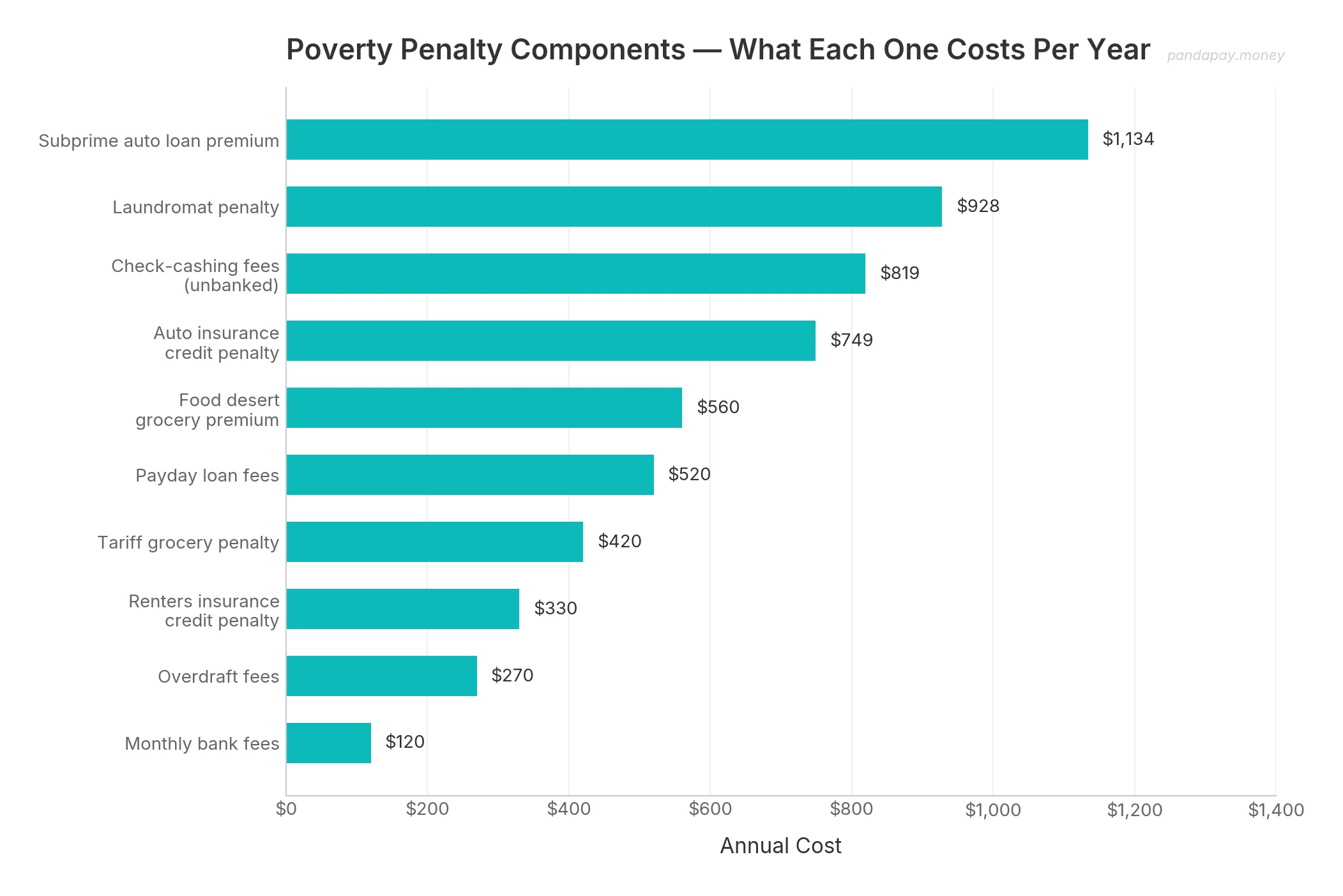

The 10 Components of the Poverty Penalty

We identified 10 distinct costs that hit households living paycheck to paycheck harder than everyone else. We organized them into three tiers based on how universally they apply.

Tier 1: Universal Penalties ($3,023/year)

These hit nearly every low-income household, regardless of specific circumstances.

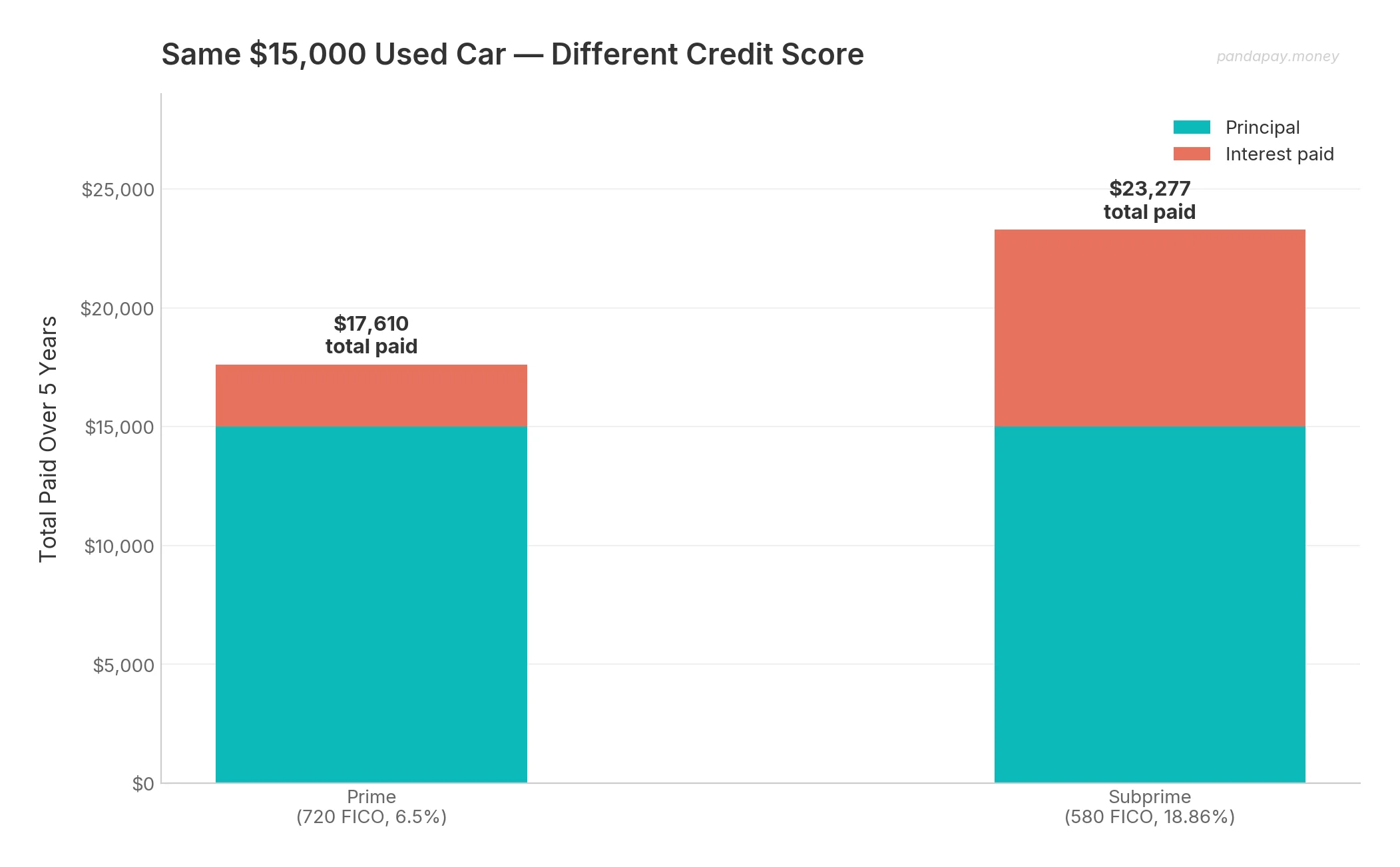

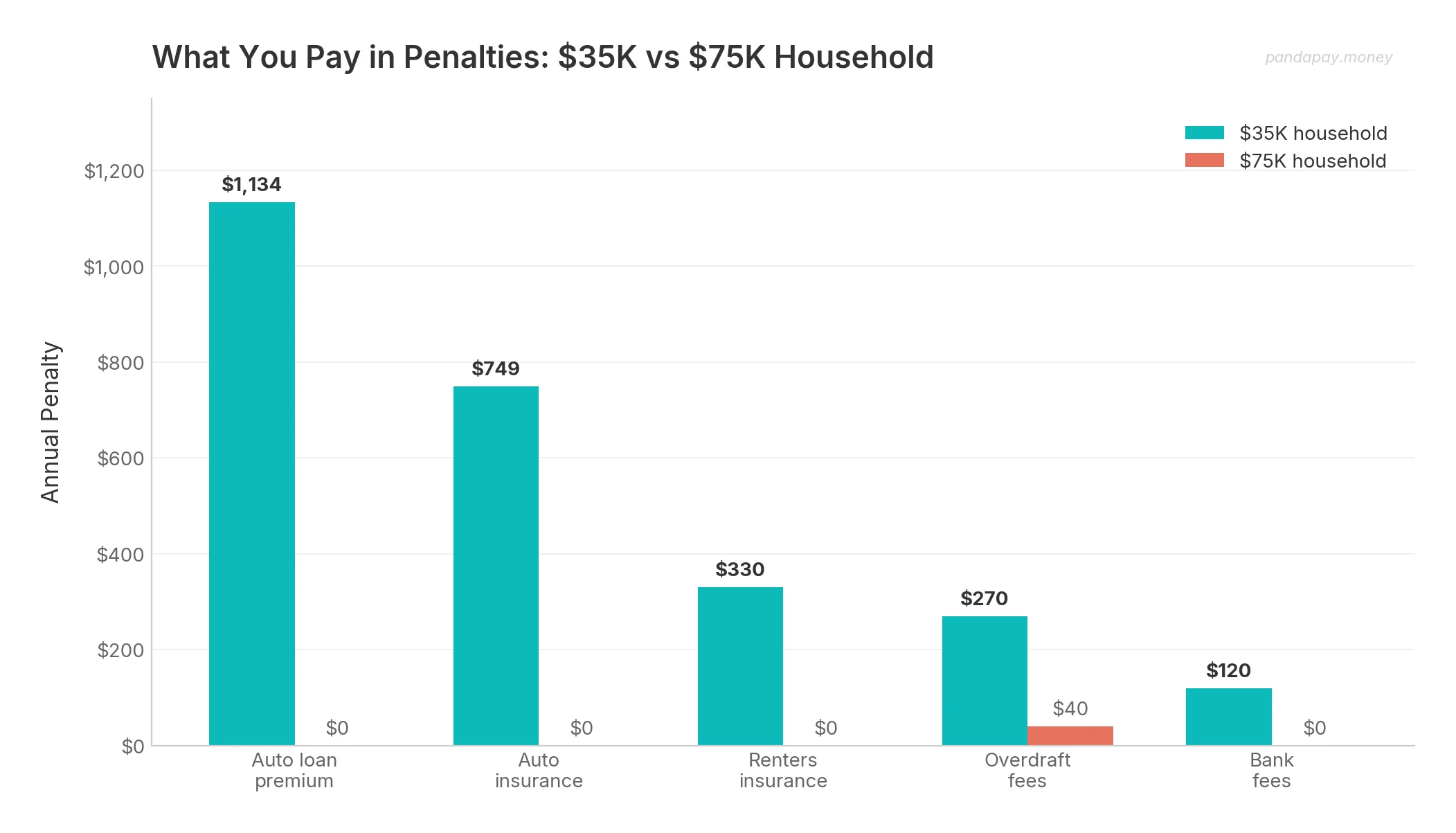

1. Subprime auto loan interest: $1,134/year

This is the largest single penalty. A $15,000 used car financed at subprime rates (18.86% average for a 580 FICO score) costs $8,277 in total interest over 5 years. The exact same car at prime rates (6.5% for a 720 FICO) costs $2,610 in interest. That's $5,668 more — $1,134 every year — for the same car on the same road.

According to Experian/TransUnion data via US News, the gap between super-prime and deep subprime on used cars can exceed 14 percentage points. At the deep subprime end (21%+), the numbers get even worse.

2. Auto insurance credit penalty: $749/year

According to Insurify's 2026 analysis, drivers with poor credit pay an average of $2,602/year for full coverage, while those with excellent credit pay $1,853. Same car. Same driving record. Same coverage. $749 more.

The penalty ranges from 40% on average up to 236% at the worst carriers — State Farm charges poor-credit drivers $609/month more than excellent-credit drivers. Only California, Hawaii, Massachusetts, and Michigan ban the practice entirely.

3. Tariff grocery penalty: $420/year

Tariffs are a regressive tax, and the Yale Budget Lab has documented exactly how regressive. The lowest income decile bears a tariff burden of 2.4% of their income — three times the rate of the top decile (0.8%). For a $35K household, the excess tariff burden over what a higher-income household pays comes to roughly $420/year.

Food prices specifically rose 2.8% from all 2025 tariff actions — roughly 1.5 times the normal annual grocery inflation rate.

4. Renters insurance credit penalty: $330/year

According to NerdWallet's 2026 analysis, renters with poor credit pay $483/year for renters insurance. Excellent credit? $153. Same apartment. Same coverage. $330 more because of a number on a report.

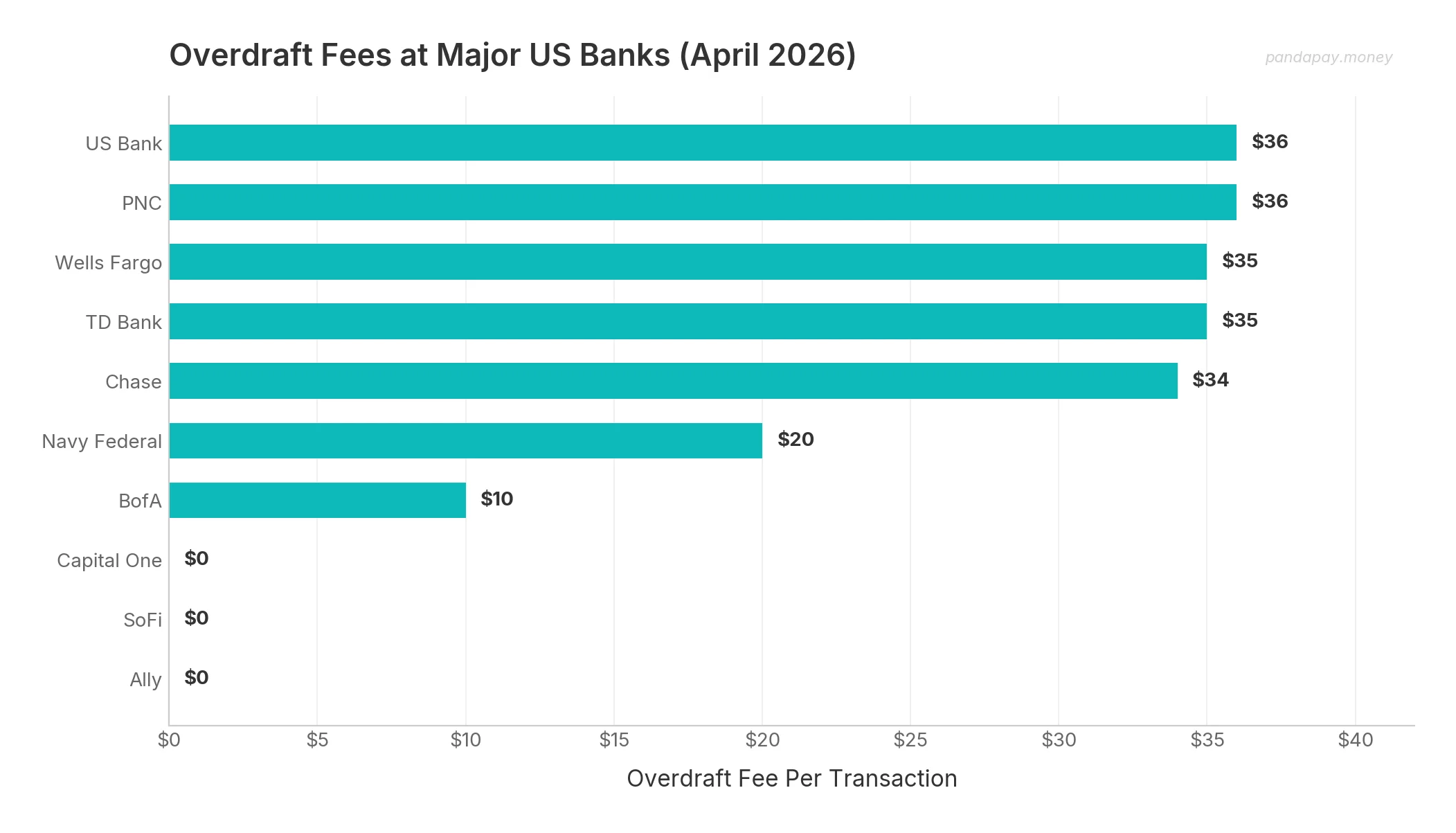

5. Overdraft fees: $270/year

We pulled fee disclosures from 20 major US banks on April 11, 2026. The results: banks that still charge overdraft fees average $29.43 per transaction. CFPB data shows that 34% of households earning under $65,000 paid at least one overdraft fee in the past year — compared to just 10% of households earning over $175,000.

Frequent overdrafters (10+ times per year) pay an average of $380/year in overdraft fees alone. We modeled a blended estimate of $270/year for the broader low-income population.

If you want to avoid overdraft fees entirely, several major banks now charge $0.

6. Monthly bank maintenance fees: $120/year

Major banks charge $7-15/month in maintenance fees, waived if you maintain a minimum balance ($500-1,500) or have qualifying direct deposits. A $35K household — roughly $1,346 biweekly after taxes — may not consistently meet those thresholds, especially in months with unexpected expenses.

Our bank-fees dataset shows Chase charges $15/month (waiver requires $500+ direct deposit or $1,500 balance), Wells Fargo charges $10/month, and US Bank charges $12/month.

Tier 2: Common Penalties ($1,488/year additional)

These hit a large subset of low-income households.

7. Laundromat penalty: $928/year

No in-unit laundry means paying roughly $5.21 per load (wash + dry + transport and supplies) instead of about $0.75 per load at home. At 4 loads per week — modest for a family — that's $1,084/year at the laundromat vs. $156 at home. A $928 penalty for not being able to afford a washer and dryer.

8. Food desert grocery premium: $560/year

The USDA documents that 11.5 million people live in low-income areas more than a mile from a supermarket. Residents pay 3-37% more for groceries at small neighborhood stores. Using a conservative 10% premium on the BLS lowest-quintile average grocery spend of approximately $5,600/year, that's $560 more for the same food.

Tier 3: Acute Penalties ($1,339/year additional)

These hit the most vulnerable — unbanked households and payday loan borrowers.

9. Check-cashing fees: $819/year

The FDIC's 2023 National Survey found that 5.6 million US households are unbanked — and check-cashing services charge an average of 2.34% per check. For a $35K annual income, that's $819/year just to access money you've already earned.

10. Payday loan fees: $520/year

According to Pew Charitable Trusts research, the average payday loan borrower spends $520 in fees to repeatedly borrow $375 — trapped in a rollover cycle where 80% of loans are taken out within two weeks of repaying the previous one.

The Total

| Tier | Annual Cost | Who It Affects |

|---|---|---|

| Tier 1 (Universal) | $3,023/year | Nearly all low-income households |

| Tier 1 + 2 (Common) | $4,511/year | Households in food deserts or without in-unit laundry |

| Full Stack (Acute) | $5,850/year | Unbanked households and payday loan users |

That's $252/month in universal costs alone. $8.28 every day.

Which Banks Still Charge Overdraft Fees in 2026?

US Bank ($36), PNC ($36), Wells Fargo ($35), TD Bank ($35), and Chase ($34) still charge overdraft fees in 2026. Capital One, SoFi, and Ally charge $0. We scraped fee disclosures from 20 major US banks on April 11, 2026 — here's the full breakdown:

| Bank | Overdraft Fee | Daily Cap | Grace Amount |

|---|---|---|---|

| US Bank | $36 | 3/day | $50 |

| PNC | $36 | 1/day | $5 |

| Wells Fargo | $35 | 3/day | $10 |

| TD Bank | $35 | 3/day | $50 |

| Chase | $34 | 3/day | $50 |

| Navy Federal | $20 | 1/day | $50 |

| Bank of America | $10 | 2/day | $1 |

| Capital One | $0 | — | — |

| SoFi | $0 | — | — |

| Ally | $0 | — | — |

The average fee among banks that still charge: $29.43 per transaction. Three out of ten charge $0.

The good news: overdraft/NSF revenue has dropped 51% since 2019 — from $11.96 billion to $5.83 billion, according to the CFPB. The bad news: the CFPB's $5 cap rule was overturned by Congress under the Congressional Review Act before it took effect. So the remaining fees at Chase, Wells, US Bank, PNC, and TD are locked in — with no regulatory floor in sight.

If you're still paying overdraft fees, switching to a $0-overdraft bank is the single easiest move on this list.

What Does a $75K Household Pay?

Roughly $800/year — compared to $3,023 for a $35K household. That's the whole point.

A $75K household typically has prime credit, easily meets bank fee waivers, rarely overdrafts, and doesn't use payday loans or check-cashing services. Their estimated universal penalty: roughly $800/year — mostly the residual tariff burden (tariffs hit everyone, just harder at the bottom).

The gap: $3,023 vs $800. The $35K household pays nearly 4x more in structural penalties.

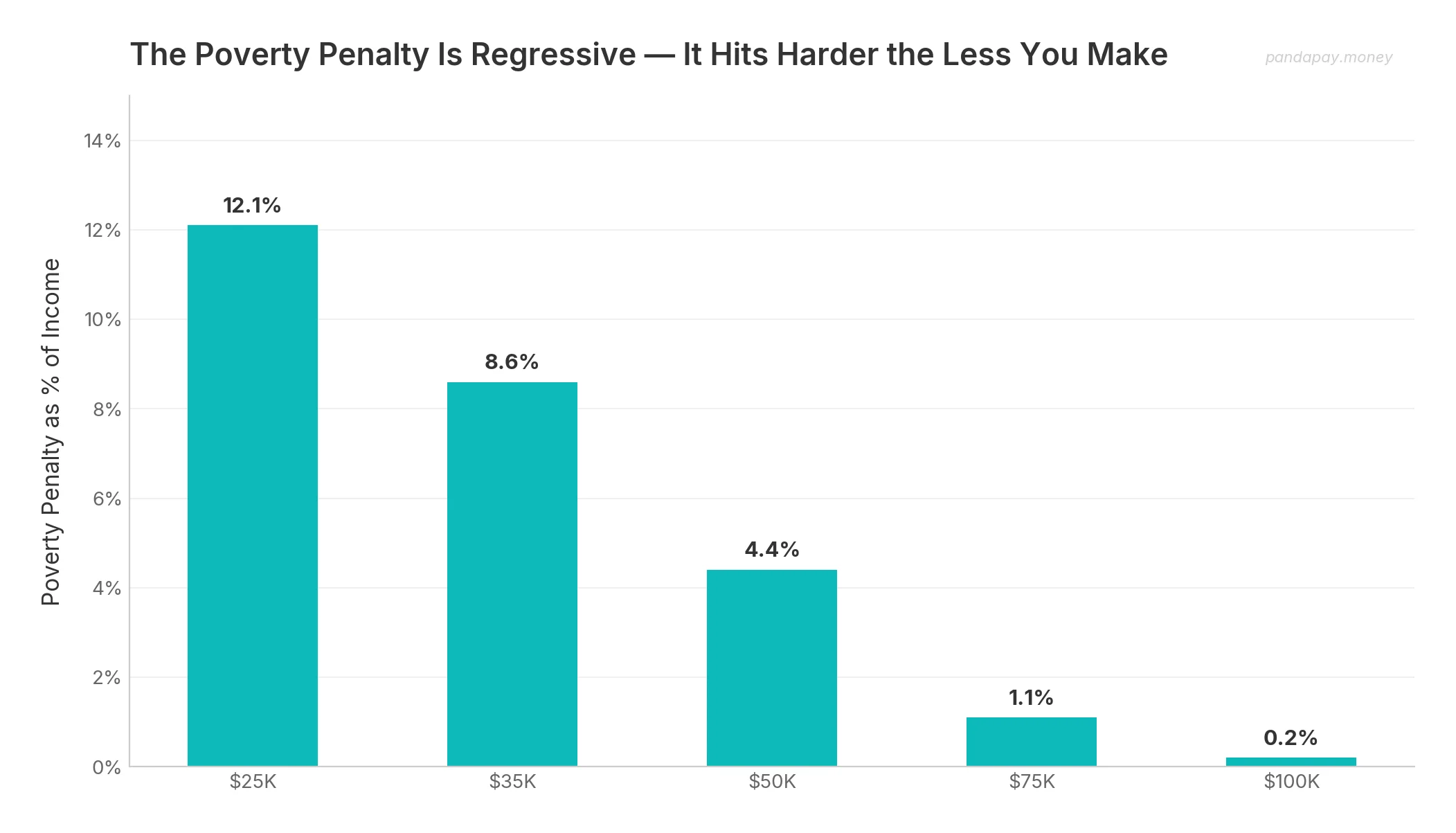

And as a percentage of income, the gap is even worse:

| Income | Universal Penalty | % of Income |

|---|---|---|

| $25K | ~$3,023 | 12.1% |

| $35K | $3,023 | 8.6% |

| $50K | ~$2,200 | 4.4% |

| $75K | ~$800 | 1.1% |

| $100K | ~$200 | 0.2% |

The less you make, the bigger the bite. That's what "regressive" means in real life.

Is the Poverty Penalty Overstated?

We went looking for the strongest counter-arguments. Three stood out.

"Overdraft fees are declining — the problem is solving itself."

Partly true. Overdraft/NSF revenue is down 51% since 2019. Capital One, Citibank, and Ally eliminated overdraft fees entirely. Bank of America dropped to $10. Mobile banking adoption among the previously unbanked grew 9x in a decade. Real progress.

But the CFPB's $5 cap was overturned. Our dataset shows five of the seven largest banks still charge $34-36 per overdraft. And frequent overdrafters — the people hurt most — still pay $380/year on average. Progress is real, but uneven.

"Not everyone faces every penalty."

Exactly. That's why we built the tier model. The $3,023 Tier 1 total includes only penalties that affect nearly every low-income household. Payday loans and check-cashing fees are in Tier 3 — we're transparent that only a subset faces those costs.

"It's about personal choices, not systems."

The Urban Institute documents that poverty itself reduces cognitive bandwidth — stress from financial scarcity literally impairs decision-making. But more fundamentally: you don't choose your credit score's effect on your auto insurance rate. You don't choose that your bank charges $34 when your account dips $7 below zero. You don't choose that tariffs hit your grocery bill three times harder.

The penalty is structural. Individual actions matter — we're about to list three that make a real difference — but the surcharge itself is baked into the system.

How Can You Stop Living Paycheck to Paycheck?

The poverty penalty is structural, but parts of it are avoidable. Here are the three highest-impact moves, ranked by savings.

1. Switch to a no-overdraft-fee bank: saves $270-380/year

Capital One, SoFi, and Ally all charge $0 for overdrafts. If you're at a bank charging $34-36 per overdraft, switching eliminates that entire cost. It takes about 30 minutes to open a new account online. If you're living paycheck to paycheck, we have a full guide to what to do when your paycheck doesn't come on time.

2. Shop auto insurance with credit-score-blind carriers: saves $200-749/year

Root, CURE, Dillo, and Lemonade skip credit checks in many states. Getting quotes from them takes 15 minutes and could save you hundreds. If you're in California, Hawaii, Massachusetts, or Michigan, credit scoring is banned entirely — but make sure your insurer isn't sneaking it in through correlated factors.

3. Refinance a subprime auto loan after 6-12 months of on-time payments: saves $500-1,134/year

Most subprime borrowers accept the rate they get at the dealership and never revisit it. After 6-12 months of on-time payments, your credit profile improves enough to qualify for meaningfully lower rates. Credit unions often offer the best refinance terms for thin-credit borrowers.

Combined potential savings: $970-2,263/year. That won't eliminate the entire penalty, but it addresses the three components you have the most control over.

For more actionable steps, see our guides on doing a subscription audit to find hidden charges and building a plan for your tax refund.

Frequently Asked Questions

How much does the poverty penalty cost per year?

We calculated that a $35,000/year household pays approximately $3,023/year in universal poverty penalties — costs like higher auto loan interest rates, insurance credit-score surcharges, overdraft fees, and regressive tariff burdens. For the most affected households (unbanked, payday loan users, food desert residents), the total can reach $5,850/year.

What is the biggest component of the poverty penalty?

Subprime auto loan interest is the single largest component at $1,134/year. A $15,000 used car at subprime rates (18.86%) costs $5,668 more in total interest than the same car at prime rates (6.5%) over a 5-year loan. Auto insurance credit penalties ($749/year) are the second largest.

Are overdraft fees still a problem in 2026?

Industry-wide overdraft revenue has dropped 51% since 2019, and several banks (Capital One, SoFi, Ally) now charge $0. But five of the seven largest traditional banks still charge $34-36 per overdraft, and the CFPB's proposed $5 cap was overturned by Congress. If you're at a bank that still charges, switching is the fastest way to eliminate this cost.

Does the poverty penalty affect everyone equally?

No. The penalty is deeply regressive — it takes 8.6% of a $35K income but only 0.2% of a $100K income. And not every low-income household faces every component. Our tier model separates universal penalties ($3,023) from common ones ($4,511) and acute ones ($5,850) to be transparent about who pays what.

Can I actually reduce my poverty penalty?

Yes. Three moves have the biggest impact: switching to a no-overdraft-fee bank (saves $270-380/year), shopping auto insurance with credit-score-blind carriers (saves $200-749/year), and refinancing a subprime auto loan after 6-12 months of on-time payments (saves $500-1,134/year). Combined potential savings: $970-2,263/year.

What Happens Next

If you're living paycheck to paycheck, the poverty penalty isn't going anywhere on its own. The CFPB's overdraft cap is dead. Credit-based insurance scoring is legal in 46 states. Tariffs are regressive by design. The structural surcharge will keep hitting the people who can least afford it — unless you take the three steps above, or unless the rules change.

We'll keep tracking. We update our bank fee disclosures quarterly, and we'll rerun this calculation every time the underlying data shifts. If you want to know what actually happens when you can't pay a bill or how to find emergency cash before payday, those guides are built on the same research rigor. Two state-specific deep dives apply the same approach to local regulatory frameworks: cash advance apps in Texas walks through the $2.03 billion Credit Access Business fee economy, and cash advance apps in Florida covers the state's strict 10%-plus-$5 payday fee cap and what that means for Floridians. And if the financial stress from the poverty penalty is also showing up in your relationship, the script to end money fights is built on the same data philosophy.

Living paycheck to paycheck costs money. Now you know exactly how much.

Appendix: Methodology

Every calculated figure in this post is sourced, dated, and auditable. Here's exactly how we got each number.

Finding: Total Annual Poverty Penalty

| Result | $3,023/year universal; up to $5,850 full stack |

| Sources | Federal Reserve SHED 2024, BLS Consumer Expenditure Survey 2024, Yale Budget Lab tariff distributional analysis (2025-2026), CFPB Overdraft/NSF Data Spotlight (Apr 2024), CFPB Frequent Overdrafters Data Point (Aug 2017), Panda Pay Data Lab bank fee disclosures (20 banks, 2026-04-11), Insurify auto insurance credit analysis (2026), NerdWallet renters insurance credit data (2026), Pew Charitable Trusts payday loan data, FDIC National Survey of Unbanked/Underbanked (2023), USDA ERS Food Access Research Atlas |

| Calculated | April 13, 2026 |

| Method | Cross-tabbed 11 primary and secondary sources to compute per-component annual costs, organized into three tiers (universal, common, acute) to avoid overstating the typical experience |

| Caveats | Not all households face every penalty. The tier model separates universal costs ($3,023) from conditional ones. Overdraft frequency uses 2017 CFPB data (most recent granular source). Insurance penalties use national averages — variation by state and carrier is significant. |

Finding: Bank-by-Bank Overdraft Fees

| Result | Average $29.43 among banks that still charge; 3 of 10 charge $0 |

| Source | Panda Pay Data Lab — bank fee disclosure scrape (20 banks targeted) |

| Date pulled | April 11, 2026 |

| Caveats | 10 of 20 banks yielded clean extraction. Citi, Chime, and Varo extraction failed (HTML parsing issues). Citizens, Fifth Third, Huntington, KeyBank, and Regions failed (access blocked or page not found). Missing banks likely split between $0 (neobanks) and $30+ (regionals). |

Finding: Subprime Auto Loan Interest Premium

| Result | $5,668 over loan life ($1,134/year) |

| Source | Experian/TransUnion Q4 2025 via US News |

| Date pulled | April 13, 2026 |

| Method | Standard amortization calculation: $15,000 principal, 60-month term, 18.86% subprime vs 6.50% prime |

| Caveats | Individual rates vary by lender, loan-to-value ratio, and debt-to-income ratio. 18.86% is the subprime used-car average; deep subprime can exceed 21%. |

Finding: Tariff Grocery Penalty by Income Decile

| Result | 2.4% of income (bottom decile) vs 0.8% (top decile) — 3x regressive |

| Source | Yale Budget Lab, "Where We Stand" |

| Date pulled | April 13, 2026 |

| Caveats | Yale Budget Lab model assumes price pass-through at the decile level. Actual household impact varies by consumption basket. |

Finding: Auto Insurance Credit-Score Penalty

| Result | $2,602 vs $1,853 — $749/year penalty (40% premium) |

| Source | Insurify 2026 analysis |

| Date pulled | April 13, 2026 |

| Caveats | National average. Varies by insurer (40-236%) and state. Banned in California, Hawaii, Massachusetts, and Michigan. |

Finding: Check-Cashing Annual Cost for Unbanked Households

| Result | $819/year (2.34% of income) |

| Source | FDIC National Survey of Unbanked/Underbanked Households (2023) |

| Date pulled | April 13, 2026 |

| Caveats | Applies only to unbanked households (4.2% of US households). |