These Banks Charge $0 for Overdrafts — Yours Probably Charges $35

We pulled the actual fee disclosures from 10 of the largest US banks. Not Bankrate's table. Not a roundup from NerdWallet. The documents the banks themselves are legally required to publish — the ones that say exactly what you'll be charged.

Three banks charge $0 for overdrafts. The rest charge $34 to $36. One switch eliminates the fee entirely.

TL;DR

- Capital One, SoFi, and Ally charge $0 for overdrafts. Chase charges $34. Wells Fargo charges $35. US Bank charges $36.

- Congress killed the $5 overdraft cap in 2025 — banks can charge whatever they want now.

- Chase collected $1.028 billion in overdraft fees in 2024. Their overdraft revenue is going up, not down.

- The annual gap is $384. That's the difference between Chase (overdraft + monthly fees) and a $0 bank — if you overdraft 6 times a year and don't qualify for fee waivers.

- Switching takes about 30 minutes. Open a new account, move your direct deposit, shift your auto-pays over 2-3 weeks.

Table of Contents

- What Every Bank Actually Charges

- The $5 Cap That Never Happened

- How Much Overdrafts Cost You Per Year

- The Grace Threshold Trick

- The 3 Banks That Charge Nothing

- How to Actually Switch (Step by Step)

- Frequently Asked Questions

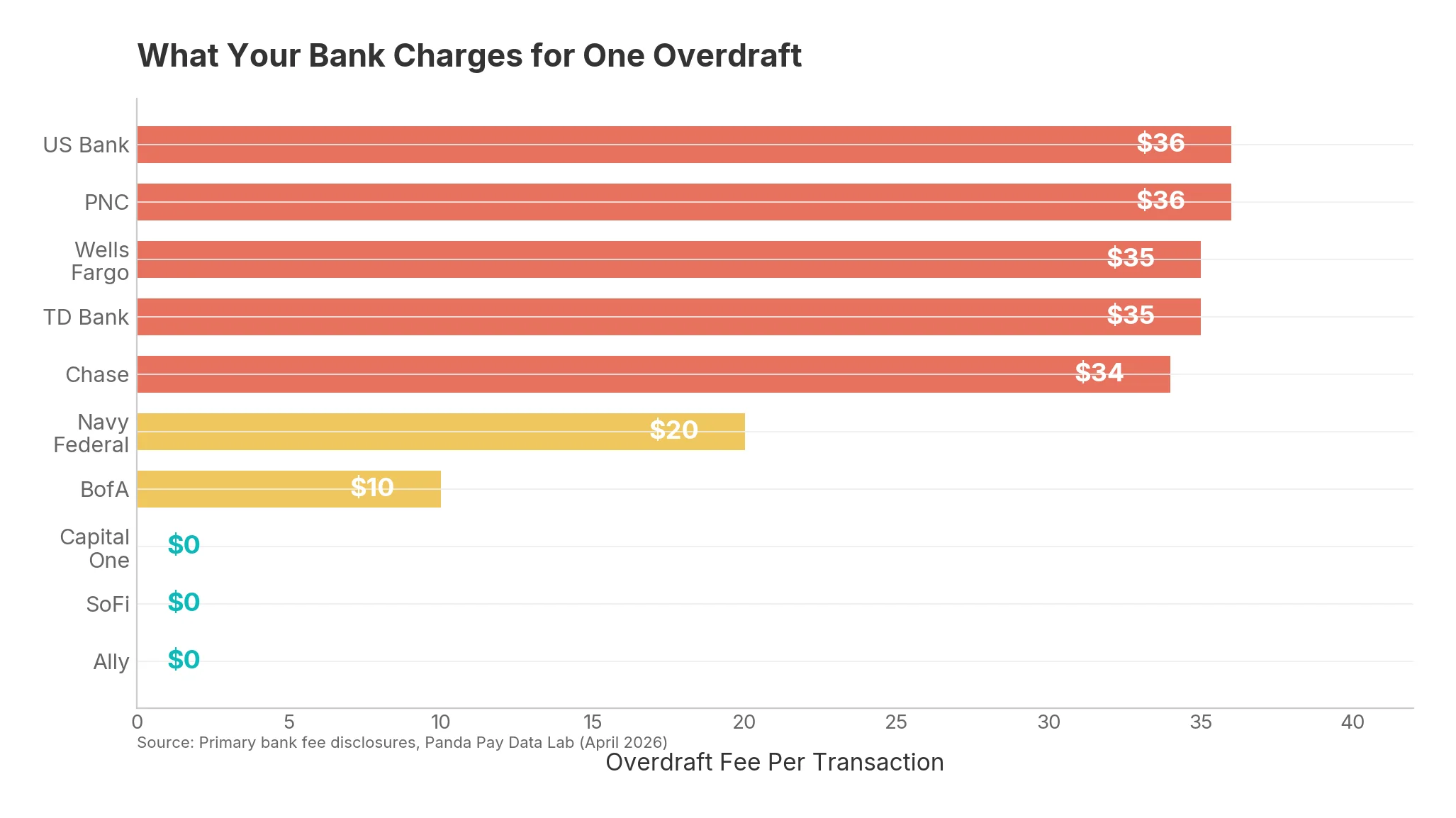

What Every Bank Actually Charges

We downloaded the fee schedule or deposit agreement from each bank's website on April 11, 2026, and extracted every overdraft-related number. Here's what we found:

The spread is enormous. US Bank and PNC charge $36 per overdraft. Chase charges $34. At the bottom: Capital One, SoFi, and Ally charge nothing.

Bank of America is the only major traditional bank that meaningfully cut its overdraft fee — down to $10, with a cap of 2 per day. Navy Federal (the largest credit union) charges $20 with a strict 1-per-day cap. Everyone else is in the $34-$36 range.

| Bank | Overdraft Fee | Daily Cap | Monthly Fee | Fee Waiver |

|---|---|---|---|---|

| US Bank | $36 | 3/day | $12 | DD $1,500+/mo or $1,500 balance |

| PNC | $36 | 1/day | $7 | $500 avg balance or DD $500+/mo |

| Wells Fargo | $35 | 3/day | $10 | DD $500+/mo or $1,500 balance |

| TD Bank | $35 | 3/day | — | — |

| Chase | $34 | 3/day | $15 | DD $500+/mo or $1,500 balance |

| Navy Federal | $20 | 1/day | $0 | None needed |

| BofA | $10 | 2/day | $12 | DD $250+/mo or $1,500 balance |

| Capital One | $0 | — | $0 | None needed |

| SoFi | $0 | — | $0 | None needed |

| Ally | $0 | — | $0 | None needed |

Every number comes from the bank's own disclosure document — downloaded and verified on April 11, 2026.

The $5 Cap That Never Happened

In December 2024, the CFPB finalized a rule that would have capped overdraft fees at $5 for banks with over $10 billion in assets. It was supposed to save consumers an estimated $5 billion a year.

It never took effect.

Congress used the Congressional Review Act to repeal it. The House voted 217-211. President Trump signed it into law as P.L. 119-10 in May 2025. The CRA also blocks the CFPB from issuing any "substantially similar" rule in the future without new congressional authorization.

The result: banks can charge whatever they want for overdrafts, and there's no federal cap coming anytime soon.

Meanwhile, Chase's overdraft fee revenue actually increased 7.66% in the first three quarters of 2025 compared to the same period in 2024, according to Consumer Federation of America analysis of FDIC Call Report data.

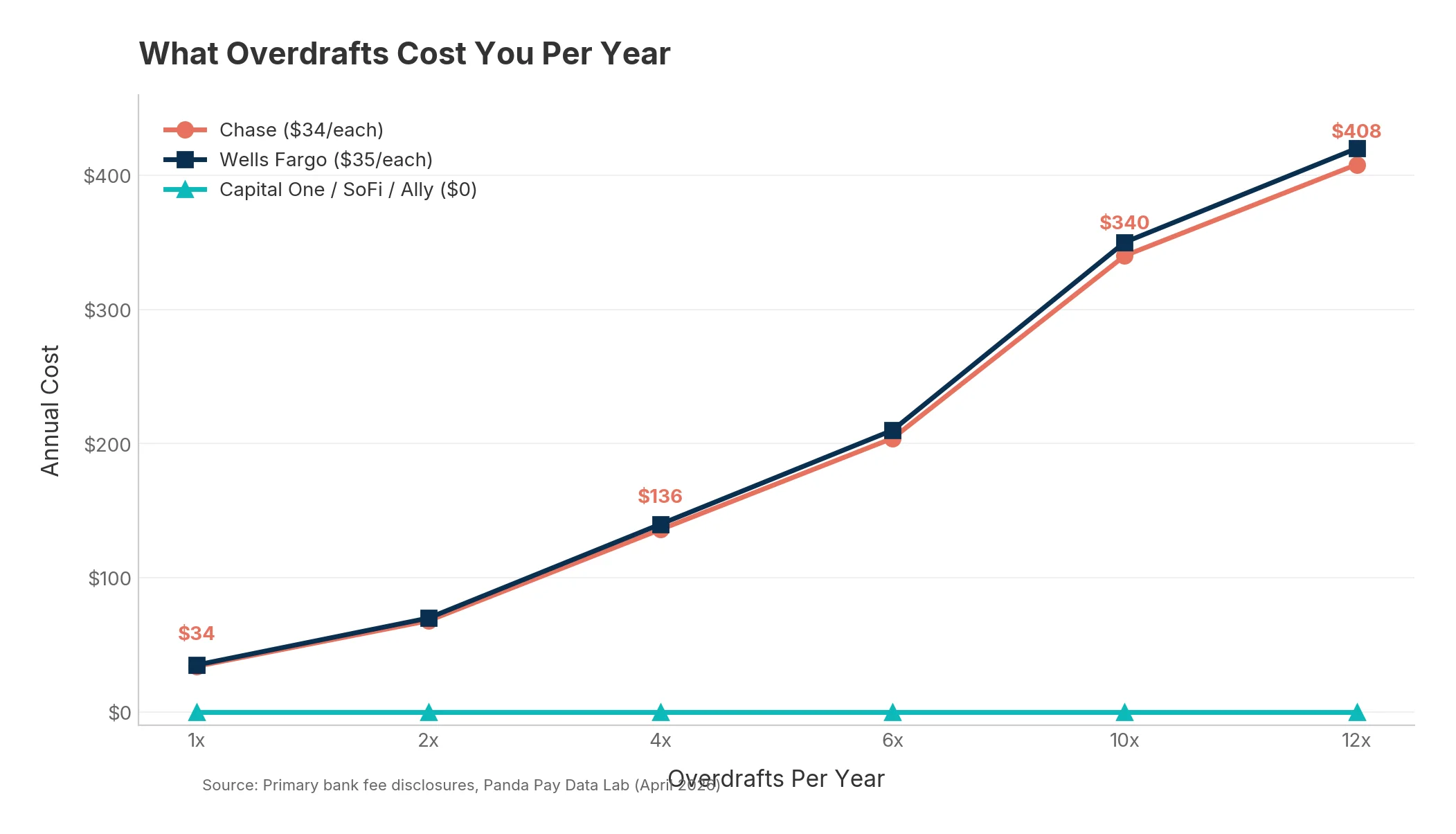

How Much Overdrafts Cost You Per Year

The average consumer who overdrafts does it multiple times a year. Here's what that costs at different frequencies:

At 6 overdrafts a year — roughly once every two months — a Chase customer pays $204 in overdraft fees alone. A Capital One, SoFi, or Ally customer pays $0.

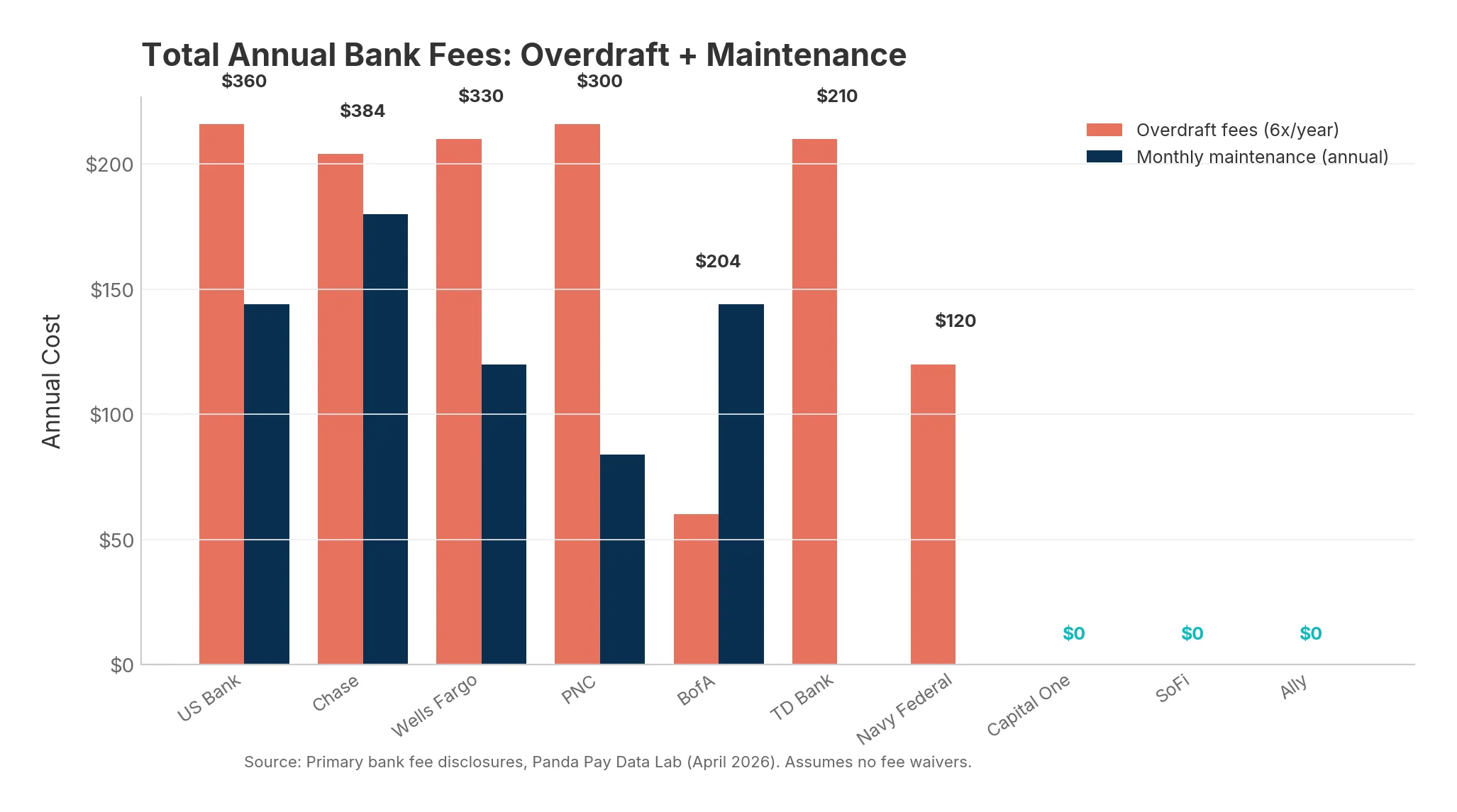

But overdrafts aren't the only fee. When you add monthly maintenance charges (assuming you don't qualify for waivers), the annual gap gets wider:

Chase customers pay up to $384/year in combined overdraft and maintenance fees. That's $32 a month that just disappears — for the privilege of having a checking account that charges you when your balance dips.

A 2025 Federal Reserve study found that credit history, more than income alone, predicts who overdrafts most — but the fix is the same either way: switch to a bank that doesn't charge.

The Grace Threshold Trick

Most banks with overdraft fees have a "grace amount" — a threshold below which they won't charge you. Sounds generous. Look closer:

- Chase: $50 grace. If you're overdrawn by $50 or less at end of business day, no fee. Cross $50.01 and it's $34.

- Wells Fargo: $10 grace. Practically useless — a single subscription charge puts you over.

- PNC: $5 grace. One coffee.

- BofA: $1 grace. Not a typo. One dollar.

The grace thresholds at Wells Fargo and BofA are so low they barely function. You'd need to overdraft by less than a fast-food meal to avoid the fee.

Capital One, SoFi, and Ally don't need grace thresholds because they don't charge the fee in the first place.

The 3 Banks That Charge Nothing

Capital One 360 Checking

- Overdraft fee: $0

- Monthly fee: $0

- Minimum balance: None

- ATM access: 70,000+ fee-free ATMs nationwide

- Bottom line: Full-service online checking with no fees across the board.

SoFi Checking & Savings

- Overdraft fee: $0

- Monthly fee: $0

- Minimum balance: None

- ATM access: Allpoint network (55,000+), no SoFi ATM fee

- Bottom line: Online-only, earns interest on checking balance, zero fees across the board.

Ally Spending Account

- Overdraft fee: $0

- Monthly fee: $0

- Minimum balance: None

- ATM access: Allpoint network, reimburses up to $10/cycle in other ATM fees

- Bottom line: Online-only, interest-earning, no fees across the board.

What You're Giving Up

Honesty check: these are online-only banks. No physical branches. If you need to deposit cash regularly or want to walk into a branch, these might not work for you. Navy Federal ($20/overdraft, $0 monthly) is the best fee option among banks with physical locations.

How to Actually Switch

Switching banks takes about 30 minutes of setup and 2-3 weeks for everything to fully move over. Here's the process:

Week 1:

- Open the new account online — Capital One, SoFi, and Ally all let you open an account in under 10 minutes with just your ID and Social Security number.

- Transfer a small buffer — Move $100-$200 to the new account so it's active.

- Update your direct deposit — Log into your employer's HR portal or payroll system and change your bank routing and account numbers. This takes 1-2 pay cycles to kick in.

Weeks 2-3: 4. Move your automatic payments to the new account — Update the bank info for each service so charges route to the new account. 5. Set up alerts — Turn on low-balance notifications on both accounts.

Week 4-8: 6. Keep the old account open — Leave a small buffer ($50-$100) in the old account for at least 60 days. Straggler charges will still hit it. 7. Close the old account — After you've confirmed everything moved, close by phone or in person. Get written confirmation.

The entire switch costs $0 and takes about 30 minutes of actual effort spread over a few weeks.

Overdraft fees are one slice of what we've called the cost of being broke in America — and the fees banks quietly brought back in 2025 don't stop at overdrafts. If your overdrafts are driven by the timing gap between paychecks and bills, state-specific options matter too: our guides to cash advance apps in Texas and cash advance apps in Florida cover what's legal locally and which small-dollar alternatives actually exist.

Frequently Asked Questions

Which banks charge $0 for overdrafts?

Capital One 360 Checking, SoFi Checking & Savings, and Ally Spending Account all charge $0 for overdrafts. Discover Cashback Debit and Chime also charge no overdraft fees. Among banks with physical branches, Navy Federal Credit Union charges $20 (the lowest among branch-based options).

How much does Chase charge for an overdraft?

Chase charges $34 per overdraft on its Total Checking account, with a maximum of 3 fees per day — meaning one bad day can cost $102 in overdraft fees alone. Chase does offer a $50 grace: if you're overdrawn by $50 or less at the end of the business day, no fee is charged. Chase collected $1.028 billion in overdraft fee revenue in 2024.

How do I switch to a bank with no overdraft fees?

Open a new account at a no-fee bank online (5-10 minutes), update your direct deposit through your employer's HR portal (takes 1-2 pay cycles), move automatic payments over 2-3 weeks by updating each recurring charge, and keep your old account open for 60 days as a buffer. Total active effort: about 30 minutes.

Did the CFPB overdraft fee cap get repealed?

Yes. The CFPB finalized a rule in December 2024 that would have capped overdraft fees at $5 for large banks. Congress repealed it using the Congressional Review Act in 2025, and President Trump signed the repeal into law (P.L. 119-10). The CRA also prevents the CFPB from issuing any substantially similar rule without fresh congressional authorization.

Are overdraft fees going down?

The average overdraft fee dropped slightly to $26.77 in 2025 (from $27.08 in 2024), according to Bankrate's annual survey. But 94% of checking accounts still charge the fee. And total consumer spending on overdraft and NSF fees actually increased to $12.1 billion in 2024, up from $11.8 billion in 2023. Some banks are charging less per incident, but consumers are paying more overall.

Related Articles

Cash Advance Apps in Florida: How They Compare to the $10/$100 Cap

Compare cash advance apps in Florida: 2026 guide to legal options, Florida's $10-per-$100 fee cap, and non-recourse alternatives for Floridians.

Cash Advance Apps in Texas: What Works in a CAB-Heavy State

Compare cash advance apps in Texas: 2026 guide to legal options, true costs (TX payday APR: 527%), and non-recourse alternatives.

7 Places That Give You Emergency Cash Before Payday (That Aren't Payday Lenders)

Need money before payday? 7 payday loan alternatives that get you emergency cash — no 400% APR. Free resources most miss.