Cash Advance Apps in Florida: How They Compare to the $10/$100 Cap

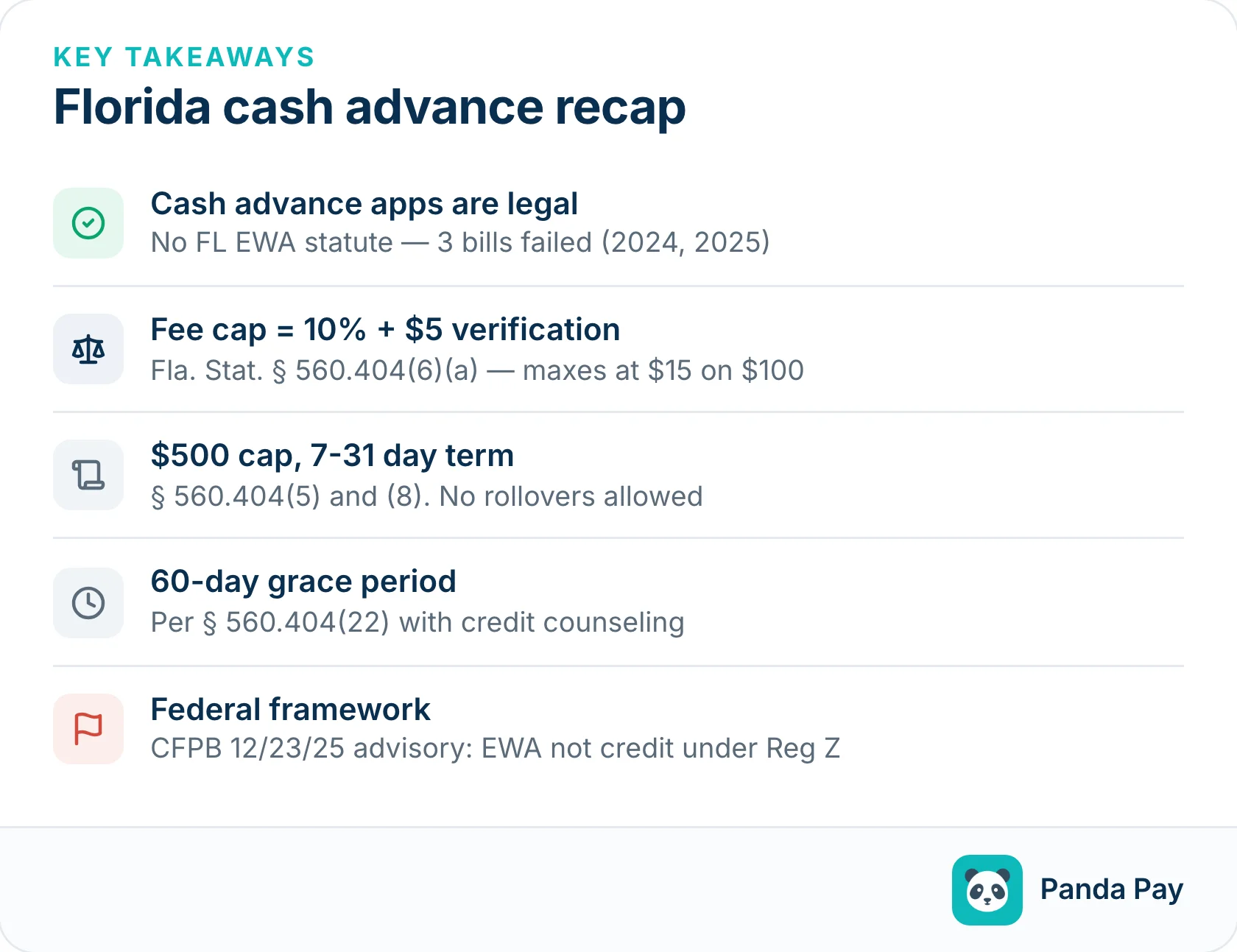

Cash advance apps in Florida operate in an unusual legal gap. The state caps payday-loan fees at 10% plus a $5 verification fee per Florida Statute § 560.404. That's one of the strongest caps in the country. But Florida cash advance laws don't cover the apps themselves. Three EWA bills have died in committee — SB 1146 in 2024, SB 422 and HB 1391 in 2025 — and no 2026 successor has been filed.

So both Florida cash advance laws and the federal CFPB framework matter if you need cash before payday. This guide covers which cash advance apps in Florida actually work, what the state's Deferred Presentment framework means for app users, and what cheaper alternatives exist. If your paycheck hasn't arrived yet, our separate guide on what to do when your paycheck doesn't come on time is a better starting point.

TL;DR

- Cash advance apps are legal in Florida. There is no Florida earned-wage-access statute as of April 2026. Three bills in three sessions have failed in the Banking and Insurance Committee.

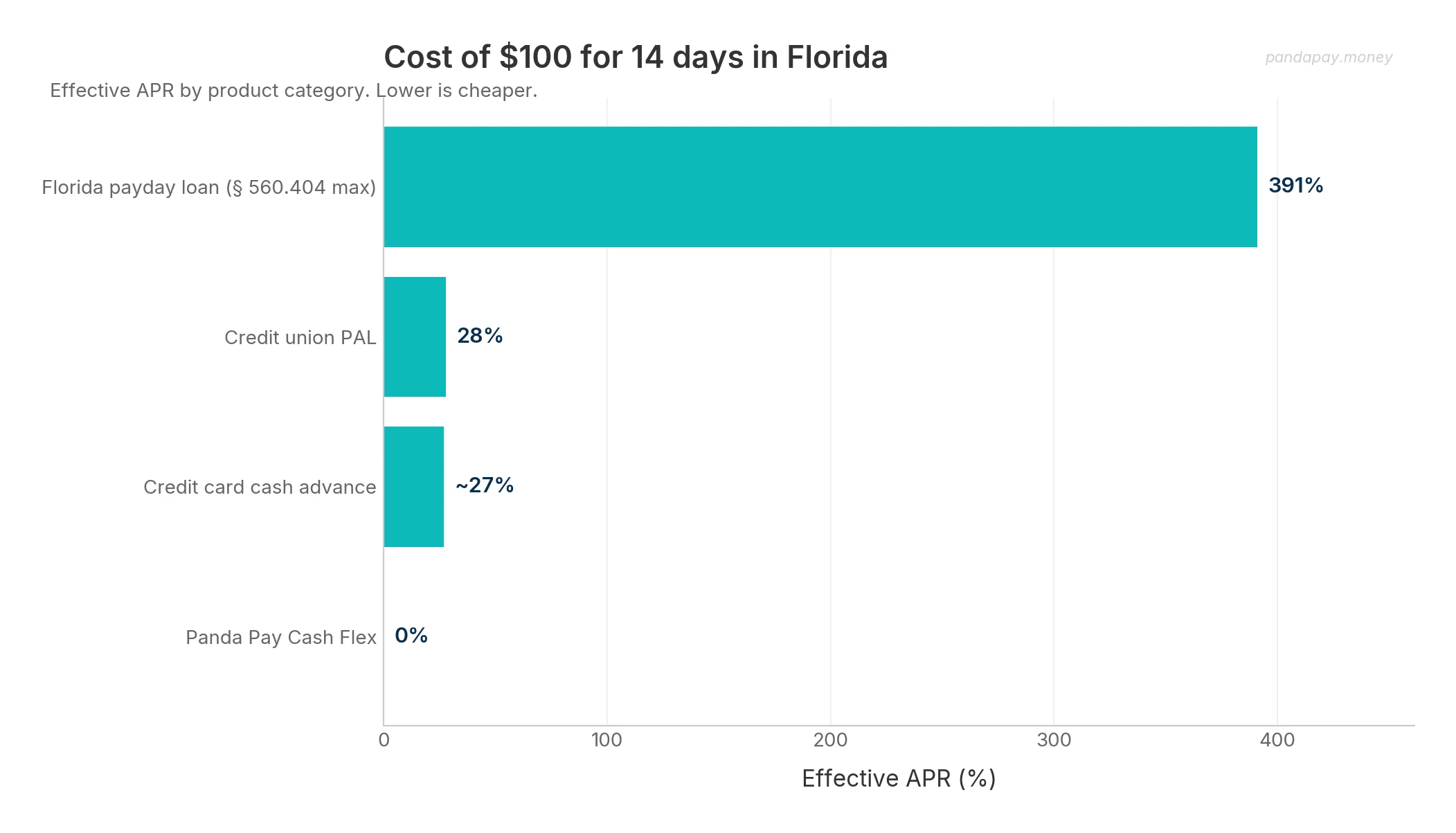

- Florida's payday loan fee cap is 10% plus $5 verification, per § 560.404(6)(a) and FAC Rule 69V-560.801. Under the cap, a $100 advance over 14 days works out to about 391% APR. A $500 advance over 14 days works out to about 287% APR.

- All 14 major cash advance apps operate in Florida. Cash advance apps are a separate product category from deferred presentment payday loans regulated under Chapter 560, Part IV.

- The CFPB's December 23, 2025 advisory opinion affirmed that qualifying earned wage access products are not credit under federal Regulation Z. It sets the federal framework for the category.

- Panda Pay's Cash Flex offers eligible Florida users up to $100 in cash flow support — no interest, no late fees, no credit check.

Table of contents

- What is Florida's Deferred Presentment framework and how do cash advance apps fit?

- Are cash advance apps legal in Florida?

- What does an instant cash advance cost in Florida under the $10-per-$100 fee cap?

- Which cash advance apps operate in Florida?

- What happened to Florida's earned wage access bill (SB 1146)?

- What are the alternatives to cash advance apps in Florida?

- How do hurricanes and disaster recovery interact with short-term cash needs in Florida?

- Are cash advance apps different for seniors, disaster survivors, or Spanish-speaking Floridians?

- Frequently asked questions

What is Florida's Deferred Presentment framework and how do cash advance apps fit?

Florida uses the Deferred Presentment framework in Chapter 560, Part IV, of the Florida Statutes (sections 560.402 through 560.408) to regulate short-term, small-dollar credit. In Florida's statute, a "deferred presentment transaction" is one where a provider gives cash in exchange for a consumer's check and agrees to hold that check for a set period. Most people call this a payday loan.

The framework is strict compared to most other payday states. § 560.404 caps single-payment advances at $500 (§ 560.404(5)) and caps the transaction fee at 10% of the amount advanced (§ 560.404(6)(a)). It also allows a separate $5 verification fee under Florida Administrative Code Rule 69V-560.801. Terms must fall between 7 and 31 days (§ 560.404(8)). Rollovers are prohibited. And § 560.404(22) requires providers to grant a 60-day grace period at no additional charge if the borrower completes consumer-credit counseling. That borrower-protection rule is unusually strong by US standards and has no equivalent in Texas.

Cash advance apps are a separate product category. The Deferred Presentment framework in § 560.402 was written for transactions where a provider holds a consumer's check for a period. That is the legal definition of a payday loan in Florida. Cash advance apps work differently. The 14 apps tracked in this guide are not registered as Florida deferred presentment providers with the Florida Office of Financial Regulation (FL OFR). The § 560.404 fee cap and 60-day grace period apply to licensed payday lenders specifically.

Are cash advance apps legal in Florida?

Yes. Cash advance apps operate legally in Florida as of April 2026. Florida has no earned-wage-access licensing statute. Three bills have died in committee in three straight sessions: SB 1146 (Sen. Jay Trumbull, died March 8, 2024, in Banking and Insurance), and SB 422 and HB 1391 (2025 session, both died June 16, 2025). No successor was filed in the 2026 session that closed on March 13.

Cash advance apps are a separate product category from deferred presentment payday loans, which are licensed by the Florida Office of Financial Regulation under Chapter 560, Part IV.

The federal framework was clarified in late 2025. On December 23, 2025, the CFPB issued a Federal Register advisory opinion. It formally affirmed that qualifying earned wage access products are not credit under Regulation Z. It also said optional expedited-delivery fees and tips on those products are not finance charges. The advisory sets the federal floor for the category as of April 2026.

What does an instant cash advance cost in Florida under the $10-per-$100 fee cap?

The Florida fee cap applies to licensed deferred presentment providers, not to cash advance apps in Florida. But it sets the benchmark Florida borrowers compare against, so the math behind an instant cash advance Florida residents can get is worth spelling out.

Under § 560.404(6)(a) and FAC Rule 69V-560.801, a single-payment deferred presentment transaction can charge up to 10% of the amount advanced plus a $5 verification fee. The table below shows the effective annual percentage rate across the allowed principal and term ranges.

| Principal | Term | 10% fee | Verification | Total fee | Effective APR |

|---|---|---|---|---|---|

| $100 | 7 days (minimum) | $10 | $5 | $15 | 782% |

| $100 | 14 days | $10 | $5 | $15 | 391% |

| $100 | 31 days (maximum) | $10 | $5 | $15 | 177% |

| $500 | 7 days (minimum) | $50 | $5 | $55 | 574% |

| $500 | 14 days | $50 | $5 | $55 | 287% |

| $500 | 31 days (maximum) | $50 | $5 | $55 | 130% |

APR = (fee ÷ principal) × (365 ÷ term days). Our calculation from the statutory fee structure.

The headline APR on a Florida payday loan depends a lot on term length. A 14-day $100 loan lands at 391% APR. The same $100 stretched to 31 days lands at 177%. The fee cap and term limits in § 560.404 apply to licensed deferred presentment providers. Cash advance apps are a separate category and structure their fees differently: express-transfer fees, optional tips, and monthly memberships.

Which cash advance apps operate in Florida?

As of April 2026, all 14 major cash advance apps operate in Florida. The table below sums up the Florida-specific terms, checked against each app's published materials.

| App | Max advance (FL) | FL registration | Subscription | Express fee | Tips | Recourse | Recent enforcement |

|---|---|---|---|---|---|---|---|

| EarnIn | $150/day, $750/pay period | Not registered | None | $2.99–$5.99 | Yes (optional) | Non-recourse | MD federal court 2025 adverse ruling |

| Dave | $500 | Not registered | $1/mo | $5 or 5%, capped $15 | Eliminated Dec 2024 | Non-recourse | FTC suit Nov 2024, DOJ referral Dec 2024 |

| Brigit | $250 | Not registered | $8.99–$15.99/mo | $0.99–$5.99 | None | Non-recourse | FTC $18M settlement Nov 2023; Feb 2026 class action |

| MoneyLion Instacash | $500 (up to $1,000 w/ RoarMoney + DD) | Not registered | $19.99/mo optional | $0.49–$8.99 | Yes (optional) | Non-recourse | NY AG suit April 2025 |

| Cleo | $250 | Not registered | $5.99–$14.99/mo | $3.99–$14.99 | None | Non-recourse | FTC $17M settlement Mar 2025 |

| Albert | $250 | Not registered | Genius $14.99–$39.99/mo | $4.99 | None | Non-recourse | None |

| Klover | $200 (to $300 via points) | Not registered | $4.99/mo optional | $1.49–$19.99 | None | Non-recourse | None |

| Tilt (ex-Empower) | $400 | Not registered | $8/mo | $1–$8 | None | Non-recourse | Rebranded Aug 2025 |

| Gerald | $100 (after BNPL purchase) | Not registered | None | None | None | Non-recourse | None |

| DailyPay | Up to 100% accrued wages | Not registered (employer EWA) | None | $3.49 instant | None | Payroll deduction | NY AG suit 2024 |

| PayActiv | ~50% accrued wages | Not registered (employer EWA) | None | $0–$3.49 | None | Payroll deduction | None |

| Possible Finance | $500 installment | Originated by Coastal Community Bank | None | $15–$25 per $100 | None | Recourse (reports to bureaus) | None |

| Chime MyPay | $20–$500/pay period | Line of Credit (Bancorp/Stride) | None | 3% of advance, capped $5 | None | Recourse (LOC) | None |

| Beem | Up to $1,000 (Everdraft) | Not registered | $2.47–$5.97/mo required | Fee for sub-8hr delivery | None | Non-recourse | None |

Two takeaways from the matrix. First, cash advance apps in Florida differ on amount, speed, and fee structure. There isn't a single "best" choice. The right pick depends on how often you'd use it and which features you need. Second, the structural model varies a lot across the category. Most operate as non-recourse advances. Possible Finance is an installment loan originated by Coastal Community Bank that reports to credit bureaus. Chime MyPay is a line of credit originated by The Bancorp Bank or Stride Bank. For comparison, our cash advance apps in Texas guide covers how the same product runs through Texas's Credit Access Business framework — a very different structural approach.

What happened to Florida's earned wage access bill (SB 1146)?

Florida cash advance laws still don't include an earned-wage-access statute. The state has tried three times to enact one, and all three attempts have failed.

SB 1146 (2024) was filed January 2, 2024, by Sen. Jay Trumbull (R-District 2, Panama City). The bill would have created the "Florida Earned Wage Access Services Act." It required EWA providers to register with the Florida Financial Services Commission through the FL OFR. It also required consumer disclosures and a no-cost disbursement option. The House companion (HB 1009, Rep. Toby Overdorf) was filed the same session. SB 1146 died March 8, 2024, in the Banking and Insurance Committee without a hearing. HB 1009 died the same day in the House Insurance & Banking Subcommittee. The bill never received a committee vote.

SB 422 (2025) was Sen. Trumbull's re-file of essentially the same bill. Filed February 28, 2025. Died June 16, 2025, in Banking and Insurance. The House companion (HB 1391, Rep. Tuck) died the same day in the Insurance & Banking Subcommittee.

The 2026 session ran from January 13 through March 13, 2026. No standalone EWA or cash advance bill was filed. Florida closed three straight sessions without enacting a framework.

Eleven states have enacted EWA-specific statutes as of April 2026: Nevada (first, 2023), Missouri, Wisconsin, Kansas, South Carolina, Arkansas, Utah, Indiana, Louisiana, Maryland, and Connecticut. Florida is not among them. Floridians rely on the federal framework from the CFPB's December 2025 advisory, plus the consumer protections in Florida's existing deferred presentment statute where they apply.

What are the alternatives to cash advance apps in Florida?

Cash advance apps are not the only short-term money option Florida residents have. Several alternatives are cheaper, slower, or structurally safer.

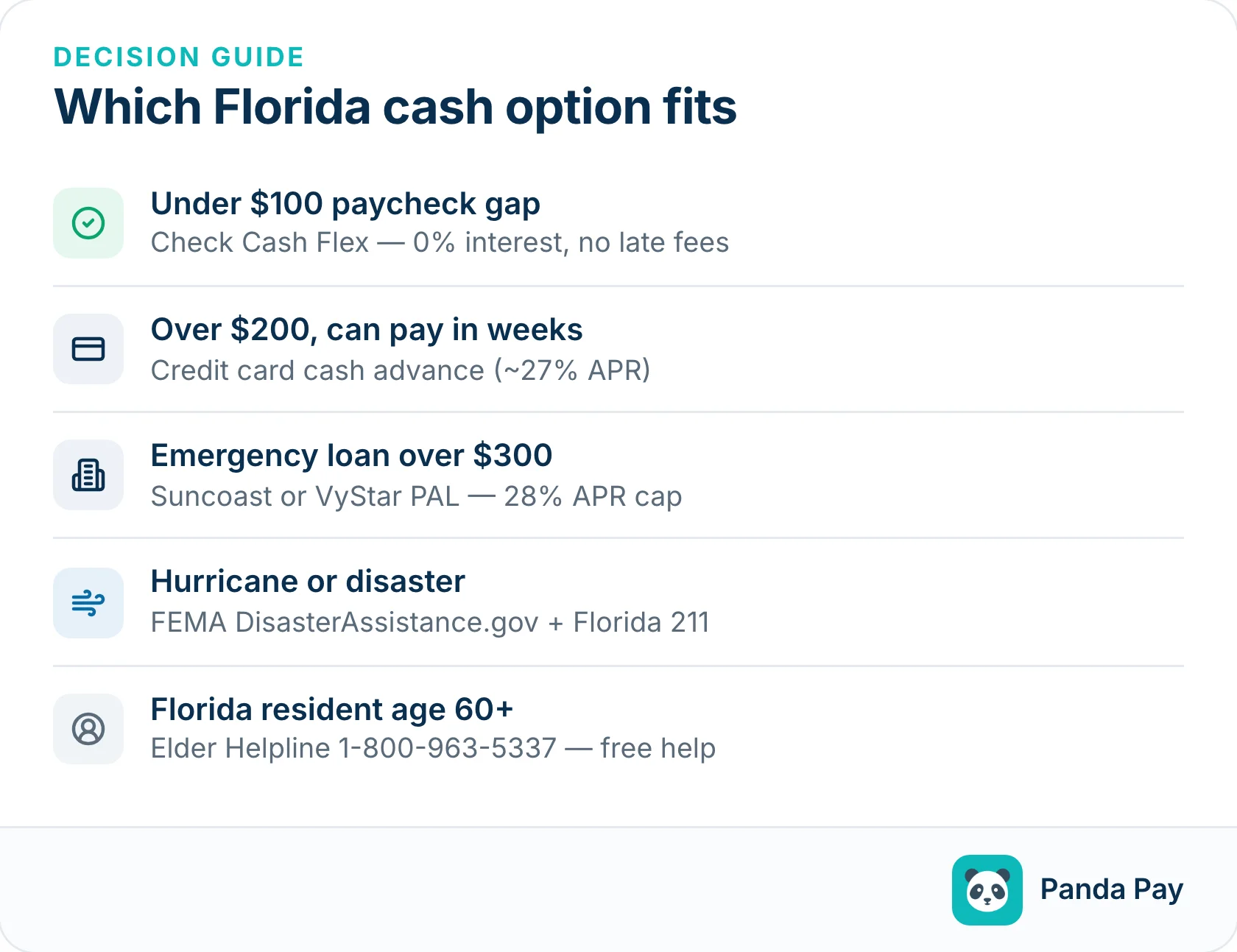

Credit union Payday Alternative Loans (PALs). The National Credit Union Administration caps PAL APRs at 28%, with a maximum application fee of $20. A $500 PAL over 6 months costs roughly $35–$40 in interest plus the application fee. Florida credit unions that offer small-dollar PALs or emergency loans include:

- Suncoast Credit Union (Tampa) — Florida's largest, 1.1M+ members

- VyStar Credit Union (Jacksonville)

- MIDFLORIDA Credit Union (Lakeland) — up to $1,000

- Space Coast Credit Union (Melbourne)

- Keys Federal Credit Union — payday-alternative product, $300–$1,000

For the national rundown beyond PALs, see our guide to payday loan alternatives.

Florida 211. Dial 2-1-1 anywhere in Florida, or visit fl211.org. The service is a nonprofit federation of 11 regional centers covering all 67 Florida counties. It's available 24/7 in 180+ languages, with in-house Spanish specialists at most South and Central Florida centers. The statewide directory includes more than 40,000 programs: utility-bill help (LIHEAP intake, Project SHARE, gas/water crisis funds), food (SNAP help, food banks, Meals on Wheels), emergency cash (Salvation Army, St. Vincent de Paul, faith-based funds), rent and eviction-prevention, and post-hurricane recovery. Nearly 1 million Floridians used Florida 211 last year.

FloridaCommerce LIHEAP and EHEAP. The Low Income Home Energy Assistance Program received $108.9 million in FY2026 federal funding for Florida. Benefit maximums are $1,350 for heating/cooling and $2,000 for year-round crisis. The Emergency Home Energy Assistance for the Elderly Program (EHEAP) is a parallel 100% federally funded track. It's run jointly by the Florida Department of Elder Affairs and the 11 regional Area Agencies on Aging, for households with at least one member age 60+.

Florida Senior Legal Helpline. 1-888-895-7873, Monday through Friday 9:00 AM to 4:30 PM ET. Free civil legal advice and referrals for Florida residents age 60 and over. Funded by the Florida Department of Elder Affairs and operated by Bay Area Legal Services.

Employer advance programs. Many Florida employers offer employer-sponsored earned wage access through DailyPay or PayActiv, especially in hospitality, retail, healthcare, and food service. Public-sector and healthcare employer partnerships are especially common in Florida because of the state's aging population and high tourism-sector employment. Ask your HR department.

Panda Pay's Cash Flex. Provides eligible Florida users up to $100 in cash flow support — no interest, no late fees, no credit check.

Credit card cash advance. Most credit cards offer cash advances at APRs of 24–29% plus a 3–5% transaction fee (minimum $10). For amounts over $200 that you can pay back soon, this is often the cheapest fast option in Florida. Interest starts from day one.

How do hurricanes and disaster recovery interact with short-term cash needs in Florida?

Florida's hurricane exposure changes the economics of short-term cash demand in a way no other state in this series faces. Four federal disaster declarations hit in 14 months between August 2023 and October 2024: Hurricanes Idalia (DR-4734-FL), Debby (DR-4806-FL), Helene (DR-4828-FL), and Milton (DR-4834-FL). FEMA approved about $89.2 million in Individual Assistance to Florida households for Helene alone, and Helene + Milton disbursements topped $1.7 billion.

FEMA Individual Assistance. Apply at DisasterAssistance.gov or 1-800-621-3362 after a federal disaster declaration. Three main components:

- Serious Needs Assistance — $770 one-time per household, available within 30 days of declaration (raised from $750 for declarations on/after Oct 1, 2024)

- Other Needs Assistance — up to $42,500 for medical, dental, childcare, transportation, moving, and funeral expenses

- Housing Assistance — separate $42,500 cap for temporary lodging, rental, repair, and replacement

Florida Small Business Emergency Bridge Loan. Up to $50,000 at 0% interest for 180 days (12% after that), for businesses with 2–100 employees in designated disaster counties. Run by FloridaCommerce. Small-business only — not an individual-borrower program.

CARE, GiveDirectly, and Red Cross. Nonprofit cash assistance after federal declarations. For Helene and Milton, GiveDirectly paid $1,000 per family to 1,636 low-income Florida families. The American Red Cross ran a joint program at $500–$750 per household. CARE paid up to $1,000 per family for Idalia in Tampa Bay. None require repayment.

Florida D-SNAP and DUA. After a federal declaration, the Florida Department of Children and Families activates Disaster SNAP — one month of emergency food benefits for non-SNAP households that otherwise qualify. Disaster Unemployment Assistance covers self-employed and gig workers who lose income.

These programs handle multi-thousand-dollar hurricane-repair needs. Cash advance apps and Cash Flex solve a different problem: small paycheck-gap shortfalls of $50–$250.

Are cash advance apps different for seniors, disaster survivors, or Spanish-speaking Floridians?

Florida residents age 65+. Florida has 5.1 million residents age 65+ (21.8% of the population — third-highest senior share nationally). The Florida Department of Elder Affairs runs the Elder Helpline at 1-800-963-5337 (M–F, 8 AM–5 PM ET), routing callers to local Area Agencies on Aging for benefits help and emergency-assistance referrals. The SHINE program (floridashine.org) offers free Medicare and Medicaid counseling. EHEAP handles utility-bill emergency help for households with a member age 60+.

Hurricane-disaster survivors. The disaster programs in the previous section pay far more than any cash advance app. A $770 FEMA Serious Needs payment, a $1,000 GiveDirectly transfer, and a one-month D-SNAP food benefit together cover more than most app advances can.

Spanish-speaking Floridians. About 22.6% of Florida households speak Spanish at home (2024 American Community Survey) — roughly 4.8 million households. Miami-Dade County is 68.8% Hispanic/Latino. Most cash advance apps in Florida offer partial Spanish interfaces but English-only fee disclosures and dispute processes. Request phone translation from FL OFR at 850-487-9687, or file through a local United Way 211 center.

Active-duty military in Florida. Florida hosts about 67,900 active-duty service members across MacDill AFB, NAS Jacksonville, NAS Pensacola, Eglin AFB, and Patrick SFB. Army Emergency Relief, Navy-Marine Corps Relief Society, and Air Force Aid Society offer 0% loans and grants for emergency needs. Each base also has its own financial readiness office.

Frequently asked questions

Are cash advance apps legal in Florida? Yes. Cash advance apps in Florida operate legally as of April 2026. The state has no EWA licensing statute. SB 1146 died in committee in 2024, and its successors SB 422 and HB 1391 both died in June 2025. No 2026 successor has been filed. Cash advance apps are a separate product category from deferred presentment payday loans, which are licensed under Chapter 560, Part IV.

What is the maximum fee on a Florida payday loan? Florida Statute § 560.404(6)(a) caps the transaction fee at 10% of the amount advanced. FAC Rule 69V-560.801 allows a separate $5 verification fee. A $100 advance can cost at most $15. A $500 advance (the statutory max) can cost at most $55. Installment deferred presentment transactions cap at 8% of the outstanding balance on a biweekly basis.

Does EarnIn work in Florida? Yes. EarnIn operates in Florida with its national caps: $150 per day and $750 per pay period. Florida is not on EarnIn's excluded-states list. Users must verify income through bank connection or workplace geolocation. A Maryland federal court denied EarnIn's motion to dismiss a usury class action in August 2025. The legal classification of EarnIn's product is still being litigated outside Florida.

Who regulates cash advance apps in Florida? The federal framework governs them. The CFPB's December 23, 2025 advisory opinion affirms that qualifying EWA products are not credit under Regulation Z. The Florida Office of Financial Regulation (FL OFR) licenses deferred presentment providers (payday lenders) under Chapter 560, Part IV — that's a separate product category.

What is Florida's 60-day grace period for payday loans? Florida Statute § 560.404(22) requires licensed payday lenders to grant a 60-day grace period at no extra charge if the borrower cannot repay. The borrower must book a consumer credit counseling appointment within 7 days after the deferment ends, and finish counseling by the end of the grace period. This protection applies only to licensed deferred presentment providers — not to cash advance apps in Florida, which sit outside Chapter 560, Part IV.

The bottom line

Florida has one of the strongest payday-loan fee caps in the United States (10% + $5 verification, per § 560.404). Cash advance apps in Florida are a separate product category — the 14 apps in the comparison table above vary a lot in fees, speed, and structure.

Before reaching for any short-term cash option, Floridians have a full set of state and nonprofit alternatives:

- Florida 211 — emergency assistance routing across all 67 counties

- LIHEAP / EHEAP — utility-bill emergency help

- Florida Department of Elder Affairs — Elder Helpline and benefits referrals

- FEMA Individual Assistance — for disaster-affected households

- Credit union PALs — small-dollar emergency loans capped at 28% APR

For small paycheck-gap needs, Panda Pay's Cash Flex gives eligible Florida users up to $100 in cash flow support — no interest, no late fees, no credit check. Download on iOS.

Related Articles

Cash Advance Apps in Texas: What Works in a CAB-Heavy State

Compare cash advance apps in Texas: 2026 guide to legal options, true costs (TX payday APR: 527%), and non-recourse alternatives.

These Banks Charge $0 for Overdrafts — Yours Probably Charges $35

We checked 10 banks' actual fee disclosures. Capital One, SoFi, and Ally charge $0 for overdrafts. Chase charges $34. Here's what switching saves you.

7 Places That Give You Emergency Cash Before Payday (That Aren't Payday Lenders)

Need money before payday? 7 payday loan alternatives that get you emergency cash — no 400% APR. Free resources most miss.