What to Actually Do When Your Paycheck Doesn't Come

Your paycheck was supposed to hit today. It didn't. Maybe your employer's payroll got delayed. Maybe you're one of the 61,000 TSA workers who went weeks without pay during the 2026 DHS funding shutdown. Maybe the math just didn't work out this time. Whatever the reason, you need a plan — not a panic spiral.

This guide covers exactly what to do: what to pay first, who to call, and how to borrow money until payday without falling into the traps that make the next paycheck even harder.

TL;DR

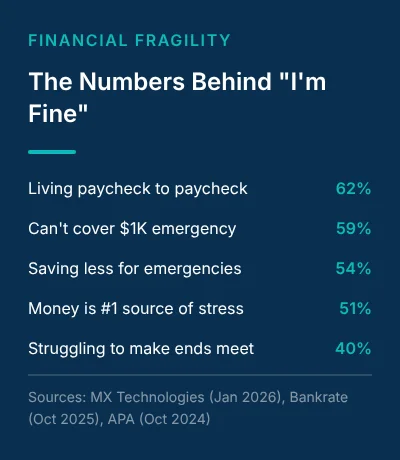

- 62% of Americans live paycheck to paycheck — a delayed or short check hits harder than most people admit

- Pay bills in this order: shelter → utilities → food → transportation → minimum debt payments → everything else

- Call before you miss — landlords, utility companies, and credit card issuers all have hardship programs most people never ask about

- Avoid payday loans at all costs — a $400 payday loan costs $646 after just 3 rollovers, and you still owe the $400

- Dial 211 for free, confidential local help with rent, food, and utilities in every U.S. state

Table of Contents

- You're Not Bad With Money — This Is Incredibly Common

- The Priority Hierarchy: What to Pay First

- Who to Call Right Now

- What NOT to Do (The Traps That Make It Worse)

- How to Borrow Money Until Payday Without Getting Trapped

- The Paycheck Gap Cycle (Why the "Fix" Becomes the Problem)

- Building a Buffer So This Doesn't Keep Happening

- Frequently Asked Questions

You're Not Bad With Money — This Is Incredibly Common

Let's get something out of the way: if your paycheck didn't cover your bills, that doesn't mean you failed at adulting. According to MX Technologies' January 2026 report, 62% of Americans live paycheck to paycheck. More than half — 59% — can't cover a $1,000 emergency from savings, per Bankrate's 2026 Emergency Fund Report.

This isn't a personal failure. It's a timing problem. The 2026 DHS shutdown made it visible when 61,000 TSA workers — federal employees with steady jobs — needed food banks to feed their families. One TSA agent told reporters: "I've done everything right and I'm asking my sister for grocery money."

And the pressure isn't getting better: in the current frozen job market of 2026, only 28% of workers think it's a good time to find a new job, meaning fewer people feel they can job-hop their way out of a bad pay week. That's why having a playbook matters even more.

Take a breath. Now let's build a plan.

The Priority Hierarchy: What to Pay First

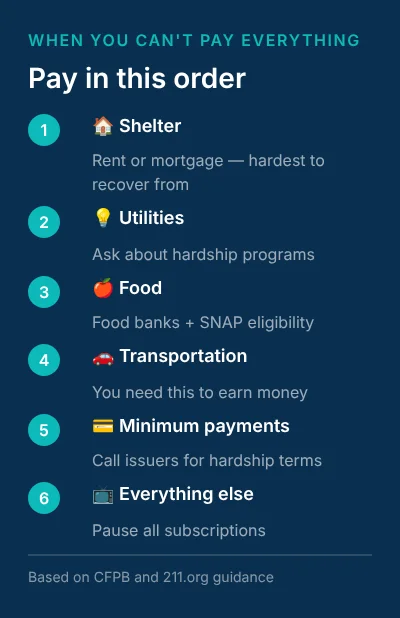

When you can't pay everything, the order matters. Not all bills carry the same consequences for being late.

Here's the framework:

1. 🏠 Shelter (rent or mortgage) Hardest to recover from if you fall behind. Call your landlord or mortgage servicer before the due date — most would rather negotiate than deal with a vacancy or foreclosure.

2. 💡 Utilities Most utility companies have formal hardship programs. They won't volunteer this — you have to ask. Call the number on your bill and say "hardship program."

3. 🍎 Food Food banks exist for exactly this situation. The USDA's SNAP program provides food assistance to eligible individuals and families. Check eligibility at benefits.gov.

4. 🚗 Transportation You need this to earn money. If you have a car payment, call your lender about forbearance. For public transit, many cities offer emergency passes — dial 211.

5. 💳 Minimum debt payments Call your credit card issuer and ask for a "hardship program." These are formal programs that can lower your minimum, pause interest, or defer payments. Banks would rather get paid late than not at all.

6. 📺 Everything else Subscriptions, gym memberships, streaming. Pause all of them. This is temporary.

Who to Call Right Now

Most people don't call anyone — they just stress silently and hope the next check fixes it. Calling is almost always better than waiting. Creditors are significantly more flexible before you miss a payment than after.

| Who | Number / Link | What to Ask |

|---|---|---|

| 211 Helpline | Dial 2-1-1 or visit 211.org | Free local help for rent, food, utilities, and more |

| Your landlord | Your lease has the number | Payment plan or temporary extension |

| Utility company | Number on your bill | "Hardship program" or "payment arrangement" |

| Credit card issuer | Number on back of card | "Hardship program" — they all have them |

| LIHEAP | liheapch.acf.gov | Federal energy bill assistance |

| Benefits.gov | benefits.gov | Check eligibility for SNAP, Medicaid, and more |

211 is the most underused resource in America. It's free, confidential, and available in every state. One call connects you with local assistance programs for rent, utilities, food, childcare, and more.

What NOT to Do (The Traps That Make It Worse)

When you're panicking about money, the fast solutions feel like lifelines. Some of them are anchors.

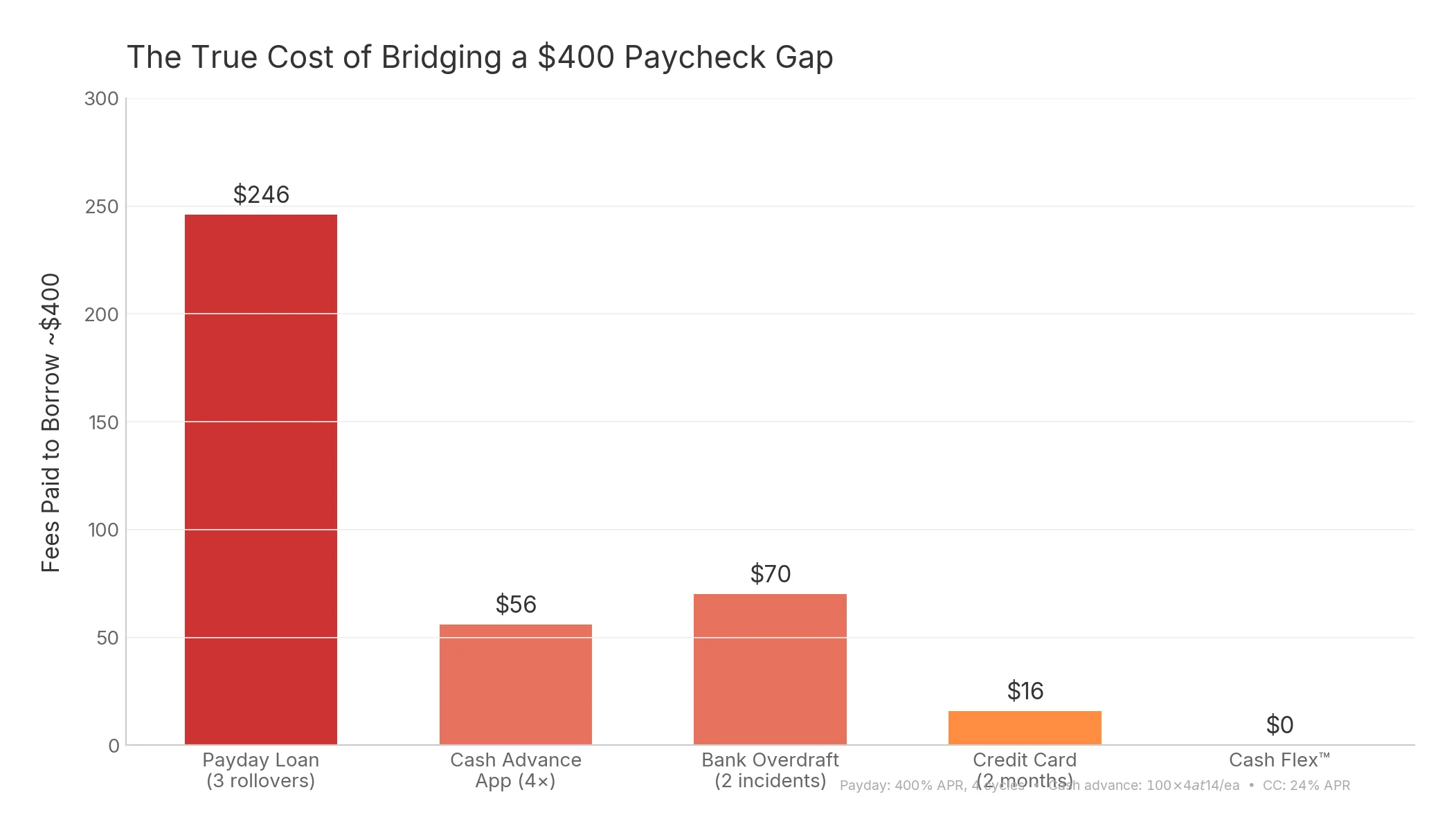

Payday Loans — The $646 Trap

A payday loan on a $400 shortfall charges roughly $61.54 per two-week cycle at the industry-typical 400% APR. According to the CFPB, 80% of payday loan borrowers roll over or renew their loan within 14 days.

After just 3 rollovers (8 weeks), you've paid $246 in fees and still owe the original $400. Total cost: $646 — 1.6 times what you needed in the first place.

Overdrafting — The Silent Fee Machine

A single $35 overdraft on a $50 shortfall costs nearly 70% of the amount you were short. Overdraft twice a month for a year and you've lost $840 — money that could have been a real emergency fund.

Draining Retirement Accounts

Early 401(k) withdrawals hit you with a 10% penalty plus income tax. A $500 withdrawal could cost $150+ in penalties and taxes. Absolute last resort.

Ignoring the Problem

Late fees stack. Credit scores drop. Landlords lose patience. Every day you wait to communicate makes recovery harder. Call before you miss, not after. If you've already missed, our what happens when you can't pay a bill day-by-day timeline lays out exactly what hits and when — it's slower than most people think, and there's more room to negotiate than you realize.

How to Borrow Money Until Payday Without Getting Trapped

If you genuinely need to bridge a gap, not every option is a trap. The key is understanding the true cost.

Here's what the numbers actually look like:

| Method | Typical Cost on $400 | Risk Level |

|---|---|---|

| Payday loan (3 rollovers) | $246 in fees | 🔴 Very high — 80% rollover rate |

| Bank overdraft (2 incidents) | $70 | 🟠 High — fees compound fast |

| Cash advance app (fee + tip) | ~$56 | 🟠 Moderate — can increase overdraft risk |

| Credit card (1 month interest) | ~$16 | 🟡 Low if paid off quickly |

| Employer pay advance | $0 | 🟢 Free — just ask HR |

| Cash flow support app (no-fee tier) | $0 | 🟢 No interest, no late fees |

Ask your employer first. Many companies offer pay advances or have partnerships with earned wage access providers. It costs you nothing and there's no interest. The worst they can say is no.

If your employer doesn't offer this, look for cash flow tools that don't charge interest, don't roll over into debt cycles, and don't penalize you for needing help. They exist — and there are more payday loan alternatives than most people realize, including free options like 211 referrals, credit union PALs, and community action agencies. If you live in Texas or Florida specifically, our state guides to cash advance apps in Texas and cash advance apps in Florida cover which apps operate locally, what the state fee caps really are, and the 211/LIHEAP/credit union options specific to each state. The table above shows the cost difference is massive.

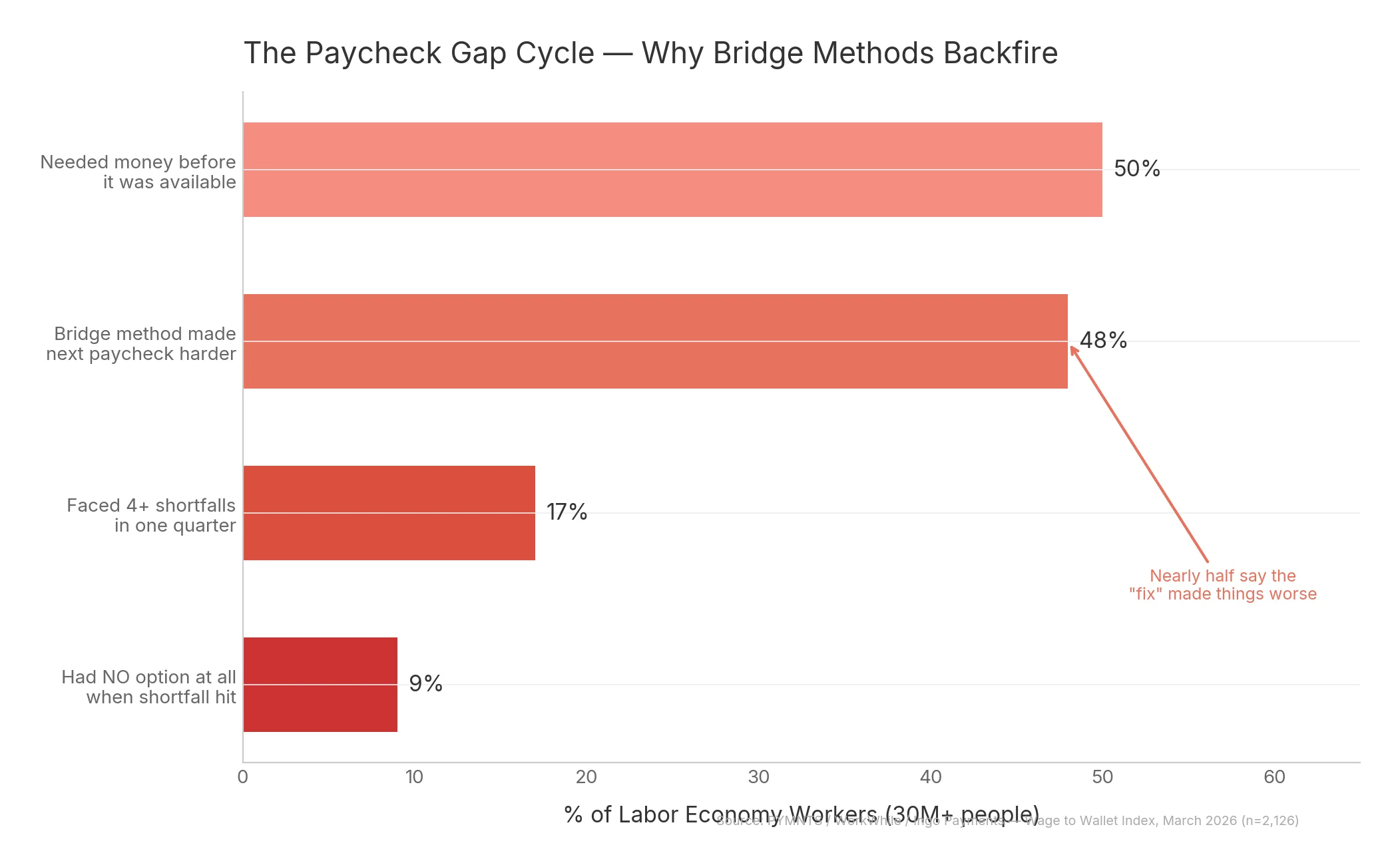

The Paycheck Gap Cycle (Why the "Fix" Becomes the Problem)

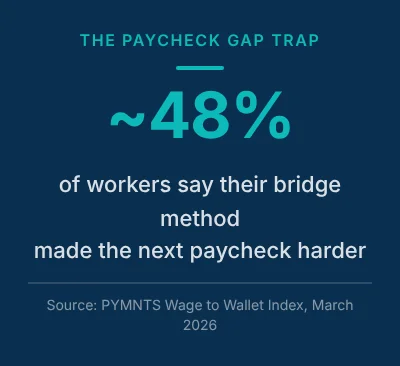

Here's the finding that should change how you think about short-term borrowing: according to PYMNTS' March 2026 Wage to Wallet Index, nearly half of workers who bridged a cash shortfall said the fix made their next paycheck harder to live on.

The math explains why. If you borrow $400 against a $1,750 net paycheck, you're now trying to cover two weeks on $1,350 — a 23% reduction. That almost guarantees another shortfall, which leads to another bridge, which leads to another reduced paycheck.

This is the cycle: miss → bridge → reduced paycheck → miss again. PYMNTS found that 17% of workers experienced 4 or more paycheck shortfalls per quarter. And 9% had literally no option when a shortfall hit — no savings, no family to call, no credit available.

The only way to break the cycle is to bridge the gap with something that doesn't eat into your next paycheck. That means either zero-cost options (employer advance, assistance programs) or cash flow support that doesn't compound with interest or rollover fees.

Building a Buffer So This Doesn't Keep Happening

Once you're through the immediate crisis, even a small buffer changes everything. You don't need $10,000 in savings. You need enough to absorb one bad week without it spiraling.

Start absurdly small. $20 per paycheck into a separate account you don't touch. After 6 months, that's $240 — enough to absorb a delayed paycheck without calling anyone.

Automate it. Set up an automatic transfer for the day after payday. If you never see the money, you won't spend it.

Know your actual number. Track what you actually spend for 30 days. The gap between perceived and actual spending is almost always larger than people expect. Spending visibility is the first step toward having a buffer.

Use tools that help, not trap. Ask yourself: does this cost me more than the problem it's solving? If a $10 fee saves you from a $35 overdraft, the math works. If it just delays the same shortfall by two weeks, it doesn't.

Frequently Asked Questions

What should I pay first if my paycheck doesn't come?

Pay in this order: shelter (rent/mortgage), utilities, food, transportation, minimum debt payments, then everything else. The key is calling each provider before you miss a payment. Most have formal hardship programs that reduce or defer payments — but you have to ask.

How can I borrow money until payday without a payday loan?

Ask your employer for a pay advance first — it's free. Beyond that, look into calling 211 for local emergency assistance, negotiating directly with creditors for extensions, or using a cash flow support app that doesn't charge interest or roll over into debt. Avoid anything with triple-digit APRs.

Why do payday loans make things worse?

The typical payday loan charges 400% APR and 80% of borrowers roll them over, according to the CFPB. A $400 loan costs $246 in fees after 3 rollovers — and you still owe the $400. The total $646 cost is 1.6 times the original need, virtually guaranteeing another shortfall.

What is the 211 hotline and how can it help?

211 is a free, confidential helpline available in every U.S. state. Dial 2-1-1 or visit 211.org to connect with local assistance for rent, utilities, food, childcare, and other emergencies. It's one of the most underused resources in the country.

Does asking for a hardship program hurt my credit score?

Generally, no. Most creditor hardship programs are internal arrangements that don't get reported to credit bureaus as negative marks. What does hurt your credit is missing payments without communicating. Calling proactively is almost always the better move for your credit and your stress level.

The Bottom Line

A missed paycheck feels like a personal emergency, but it's actually one of the most common financial events in America. 62% of Americans live paycheck to paycheck — you're not uniquely bad at this.

The playbook is straightforward: prioritize your bills (shelter first, subscriptions last), call everyone before you miss a payment, avoid payday loans and overdraft spirals, and bridge the gap with the lowest-cost option available to you.

If you need breathing room right now, start with 211. It's free, it's confidential, and it connects you with help that's already there — you just have to ask.