Cash Advance Apps in Texas: What Works in a CAB-Heavy State

Texans paid roughly $2.03 billion in Credit Access Business fees in 2024, per the Texas Office of Consumer Credit Commissioner. That number is the backdrop for why cash advance apps have exploded in Texas. It's also why the category is more complicated here than in any other US state.

This guide covers which apps actually work in Texas as of April 2026. It explains what the state's Credit Access Business (CAB) model means for you. And it shows how the costs really compare. If your paycheck hasn't arrived yet, our separate guide on what to do when your paycheck doesn't come on time is a better starting point.

TL;DR

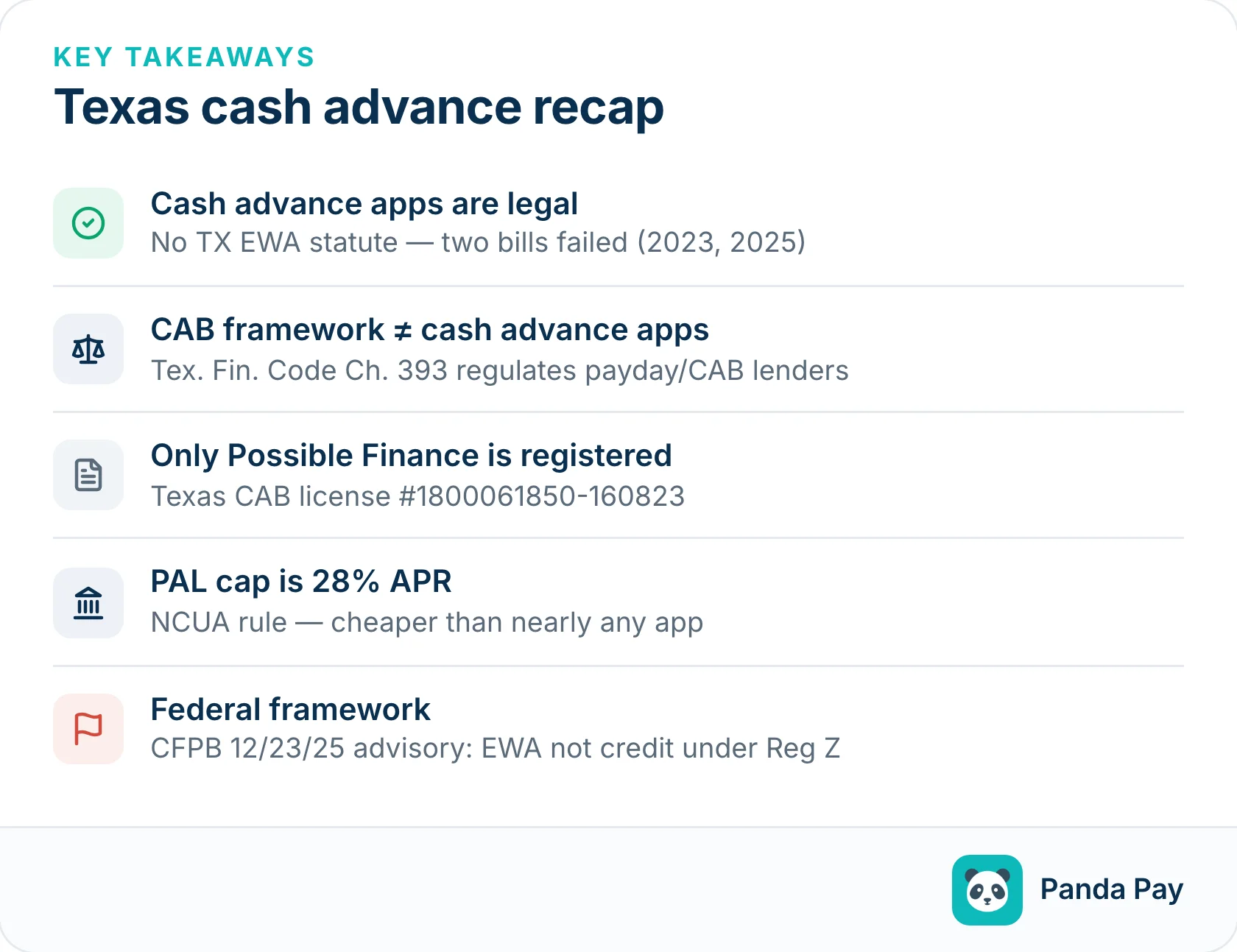

- Cash advance apps are legal in Texas. Texas has no earned-wage-access licensing law as of April 2026. Two proposed bills died in committee, most recently in the 89th Legislature (2025).

- Texas is a high-payday-APR state. The average APR on a $500 four-month installment payday loan is 527%, per Pew Charitable Trusts. Cash advance apps are a separate product category from Texas's payday lenders.

- Possible Finance is the only major app registered as a Texas CAB (license #1800061850-160823). Other apps operate as a different product category.

- The CFPB's December 23, 2025 advisory opinion affirmed that qualifying earned wage access products are not credit under federal Regulation Z. It sets the federal framework for the category.

- Panda Pay's Cash Flex offers eligible Texas users up to $100 in cash flow support — no interest, no late fees, no credit check.

Table of contents

- What counts as a cash advance app in Texas?

- Are cash advance apps legal in Texas?

- How does Texas's Credit Access Business (CAB) system work?

- Which cash advance apps actually work in Texas?

- What does an instant $100 cash advance cost in Texas?

- What are the alternatives to cash advance apps in Texas?

- Are cash advance apps different for military, gig workers, or fixed-income Texans?

- Frequently asked questions

What counts as a "cash advance app" in Texas?

A cash advance app is a smartphone app that gives you small amounts of money before your next paycheck — typically $50 to $500. In return, you pay some mix of a subscription fee, an express transfer fee, or an optional "tip." Three business models exist:

- Direct-to-consumer apps — Dave, Brigit, Cleo

- Employer-partnered earned wage access — DailyPay, PayActiv

- Buy-now-pay-later hybrids — Gerald

These apps are different from payday loans, which are short-term consumer loans regulated in Texas through the Credit Access Business (CAB) framework. They're also different from credit card cash advances, which are extensions of credit on a credit card under federal Regulation Z. And they're not quite the same as earned wage access (EWA) in the strict sense. True EWA is employer-sponsored and tied to payroll records of earned-but-unpaid wages, which most direct-to-consumer apps don't have.

The category matters because Texas regulates each of these differently. Payday loans are licensed under the CAB framework in Texas Finance Code Chapter 393. Earned wage access is governed by the federal framework from the CFPB's December 23, 2025 advisory opinion. That advisory affirms that qualifying EWA products are not credit under Regulation Z.

Are cash advance apps legal in Texas?

Yes. Cash advance apps operate legally in Texas as of April 2026. The state has no earned-wage-access licensing statute. Two proposed bills (HB 3827 in 2023 and HB 2043 in 2025) failed in committee. Cash advance apps are a separate product category from payday loans, which are regulated under the Texas Credit Access Business framework.

The federal framework was clarified in late 2025. On December 23, 2025, the CFPB issued a Federal Register advisory opinion. It formally affirmed that qualifying earned wage access products are not credit under Regulation Z. It also said optional expedited-delivery fees and tips on those products are not finance charges. The advisory sets the federal floor for the category as of April 2026.

How does Texas's Credit Access Business (CAB) system work?

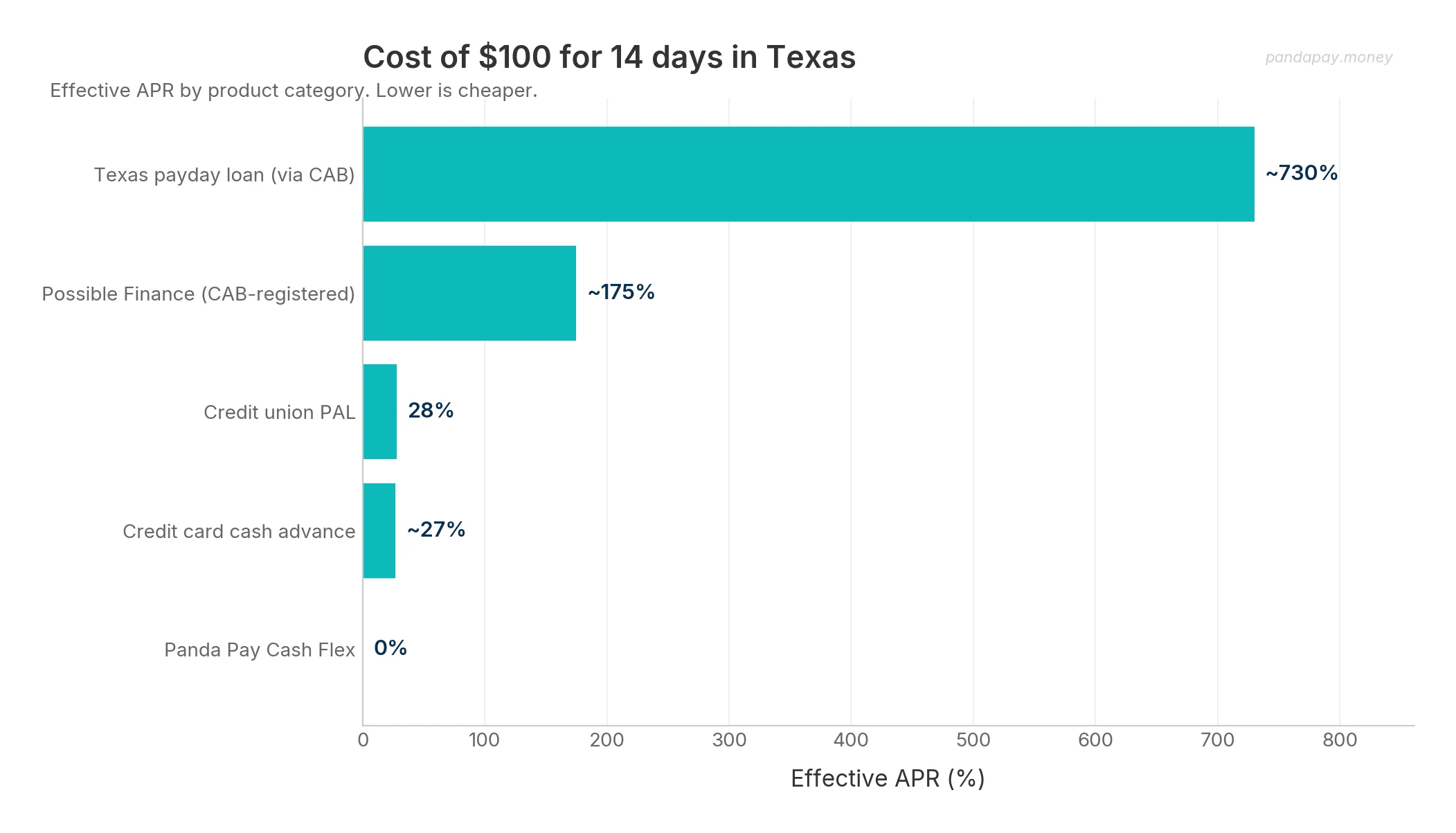

A Credit Access Business is a Texas-specific legal entity defined in Texas Finance Code Chapter 393, Subchapter G. A CAB is a broker that arranges a consumer loan from a third-party lender and charges its own fee for the arrangement. The third-party lender's interest stays at or below Texas's 10% usury cap. The CAB's broker fee — typically $22 to $28 per $100 borrowed per two-week term — is legally counted as a service charge rather than interest.

The result is that Texas has no meaningful cap on small-dollar consumer credit costs. Pew Charitable Trusts calculated Texas's average APR on a $500 four-month installment payday loan at 527%. That's behind only Utah, Nevada, and Idaho. In CY 2024, 1,524 licensed CABs collected about $2.03 billion in fees from Texas consumers — across single-payment payday, installment payday, and auto-title products combined. Per the OCCC's annual CAB report.

Possible Finance is the notable exception among major cash advance apps. It holds Texas CAB license #1800061850-160823 and operates as a licensed small-dollar installment lender. Its loans are originated by Coastal Community Bank. Possible's disclosed APR is 150–200% — fully transparent and reported to two credit bureaus as installment payments.

Which cash advance apps actually work in Texas?

As of April 2026, all twelve major cash advance apps operate in Texas, though product details vary. The table below sums up the Texas-specific terms, checked against each app's published materials.

| App | Max advance (TX) | TX CAB status | Subscription | Express fee | Tips | Recourse | Recent enforcement |

|---|---|---|---|---|---|---|---|

| EarnIn | $150/day, $750/pay period | Not registered | None | $2.99–$5.99 | Yes (optional) | Non-recourse | MD federal court 2025 adverse ruling |

| Dave | $500 | Not registered | $1/mo | $5 or 5%, capped $15 | Eliminated Dec 2024 | Non-recourse | FTC suit Nov 2024, DOJ referral |

| Brigit | $500 | Not registered | $8.99–$14.99/mo | $0.99–$5.99 | None | Non-recourse | FTC $18M settlement Nov 2023 |

| MoneyLion Instacash | $500–$1,000 | Historical CAB (surrendered) | $19.99/mo optional | $0.49–$8.99 | Yes (optional) | Non-recourse | NY AG suit 2024 |

| Cleo | $250 | Not registered | $5.99–$14.99/mo | $3.99–$14.99 | None | Non-recourse | FTC $17M settlement Mar 2025 |

| Albert | $250 | Not registered | Genius $39.99/mo | $6.99 | None | Non-recourse | None |

| Klover | $200 | Not registered | $4.99/mo optional | $1.49–$19.99 | None | Non-recourse | None |

| Tilt (ex-Empower) | $400 | Not registered | $8/mo | $1–$8 | None | Non-recourse | Rebranded Aug 2025 |

| Gerald | $200 (after BNPL purchase) | Not registered | None | None | None | Non-recourse | None |

| DailyPay | Up to 100% accrued wages | Not registered (employer EWA) | None | $3.49 instant | None | Payroll deduction | NY AG suit 2024 |

| PayActiv | ~50% accrued wages | Not registered (employer EWA) | None | $0–$3.49 | None | Payroll deduction | None |

| Possible Finance | $500 installment | CAB #1800061850-160823 | None | $15–$25 per $100 | None | Recourse (reports to bureaus) | None |

Two takeaways from the matrix. First, only Possible Finance is registered with the Texas OCCC as a Credit Access Business. It's the one app with fully disclosed APR (150–200%) and bureau-reported repayment. Second, the employer-sponsored EWA products (DailyPay, PayActiv) are only available if your Texas employer has already partnered with them. They are not direct-to-consumer options.

What does an instant $100 cash advance cost in Texas?

A $100 cash advance in Texas typically costs $0 to $22 in fees over a two-week cycle, depending on the provider. Express fees range from roughly $2.99 to $8 for instant transfer. Standard 1-3 day transfers are usually free. Most apps also charge a monthly subscription — check the per-app figures in the comparison table above.

A few factors drive total cost:

- Express fees. Nearly every app charges a separate fee for instant transfer (minutes) vs standard transfer (1-3 business days). Gerald is the exception: no express fee, but cash advances are gated behind an in-app BNPL purchase first.

- Subscription. Monthly subscription fees vary widely, from $1 at Dave to $39.99 at Albert's Genius tier. Gerald and DailyPay have no subscription. PayActiv is employer-paid.

- Credit card cash advance. If you have a credit card with available credit, a cash advance runs 24-29% APR plus a 3-5% transaction fee (minimum $10). For amounts above $200, this is often the cheapest fast option. Interest starts from day one. There's no grace period.

What are the alternatives to cash advance apps in Texas?

Cash advance apps are not the only short-term money option Texans have. Several alternatives are cheaper, slower, or structurally safer.

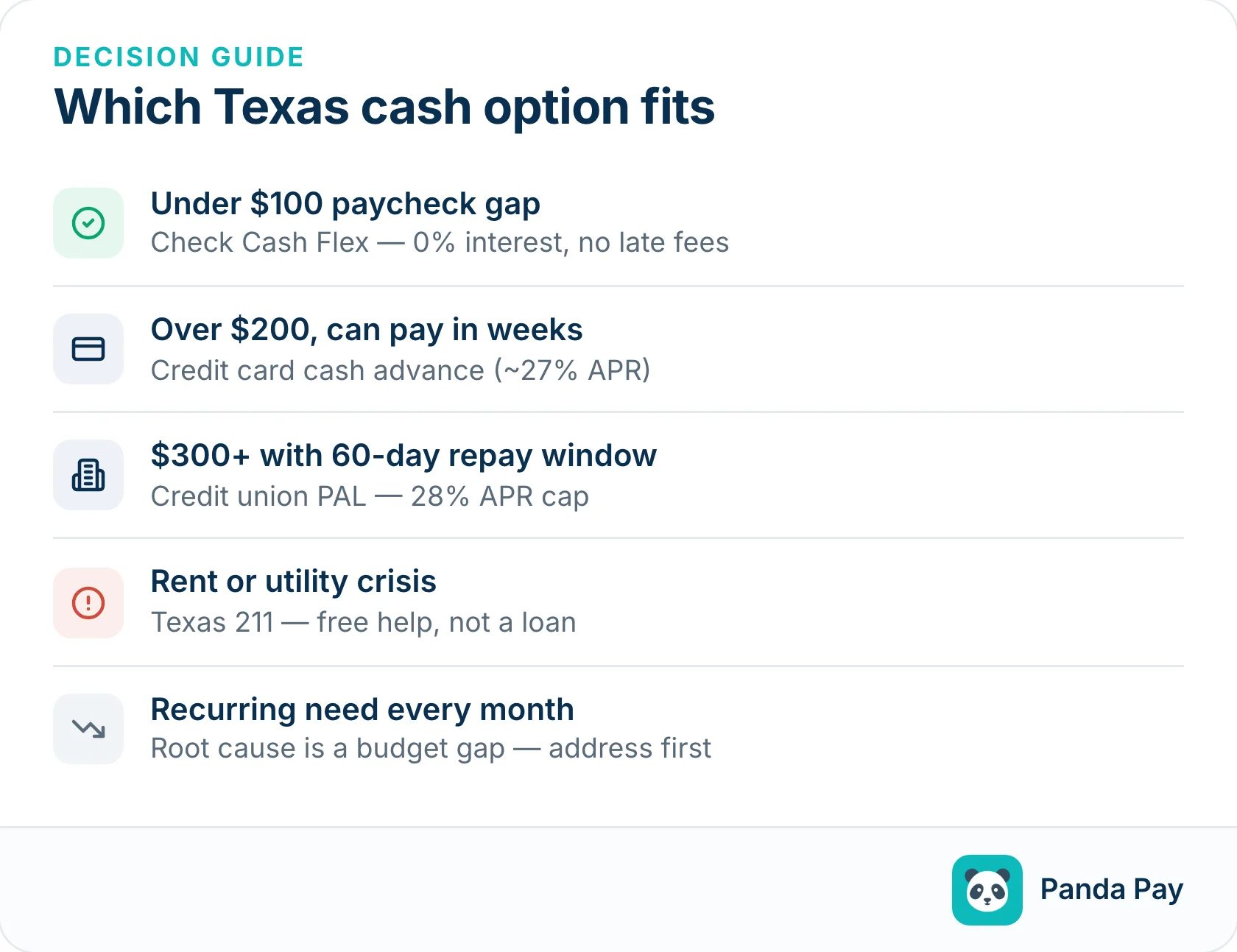

Credit union Payday Alternative Loans (PALs). The National Credit Union Administration caps PAL APRs at 28%, with a maximum application fee of $20. Texas credit unions that offer PALs include GECU (El Paso), Security Service Federal Credit Union (San Antonio), Randolph-Brooks FCU, and others. A $500 PAL over 6 months costs roughly $35–$40 in interest plus the app fee. For the full national rundown beyond PALs, see our guide to payday loan alternatives.

Texas 211. The statewide 211 service (211texas.org) refers callers to emergency help for rent, utilities, food, and prescriptions — often free. United Way, local church networks, and Texas Health and Human Services route through 211. The Low Income Home Energy Assistance Program (LIHEAP / CEAP) can free up rent money by covering utility bills directly.

Employer advance programs. Many Texas employers offer some form of payroll advance, especially hourly-wage employers (retail, healthcare, food service). Kroger, HEB, major hospital systems, and most large Texas employers partner with DailyPay or PayActiv. Ask HR whether your paycheck is eligible.

Panda Pay's Cash Flex. Provides eligible users up to $100 in cash flow support — no interest, no late fees, no credit check.

Credit card cash advance. Most credit cards offer cash advances at APRs around 24–29% with a 3–5% transaction fee (minimum $10). For amounts over $200 you can pay back soon, this is often the cheapest fast option. Interest starts from day one. There's no grace period.

Are cash advance apps different for military, gig workers, or fixed-income Texans?

Active-duty military on Texas bases. About 100,000 service members serve at Fort Hood (formerly Fort Cavazos), Fort Bliss, Joint Base San Antonio, NAS Corpus Christi, and other Texas bases. Army Emergency Relief, Navy-Marine Corps Relief Society, and Air Force Aid Society offer 0% loans and grants for emergency needs. Each base also has its own financial readiness office.

Gig workers across Texas metros. About 2.5–3 million Texans are gig or 1099 workers — DoorDash, Uber, Lyft, Instacart, and Favor drivers concentrated in Houston, Dallas, Austin, and San Antonio. The common problem: most cash advance apps require verified direct deposit from a recognizable employer, but gig income arrives as irregular micro-deposits from multiple platforms. Dave and MoneyLion are friendlier here because they underwrite on overall bank flow. EarnIn requires workplace geolocation or employer verification, which gig workers can't always supply.

Fixed-income and SSI recipients. Many Texans on Social Security, SSDI, or VA benefits have shortfalls in the $40 to $120 range between benefit payments. Cash Flex's $100 cap matches the actual size of most fixed-income shortfalls better than larger advance products. The Texas Health and Human Services benefits navigator at yourtexasbenefits.com and Texas 211 can connect fixed-income residents to emergency-assistance programs they may not know about.

Spanish-speaking Texans. About 40% of Texans are Hispanic, and metros like McAllen-Edinburg-Mission are over 90% Hispanic. Most cash advance apps offer partial Spanish interfaces but English-only fee disclosures and dispute processes. The OCCC publishes consumer complaint forms in Spanish at occc.texas.gov.

Frequently asked questions

Are cash advance apps legal in Texas? Yes. Cash advance apps operate legally in Texas as of April 2026. Texas has no earned-wage-access-specific licensing statute — proposed bills in 2023 and 2025 did not pass. Cash advance apps are a separate product category from payday loans, which are licensed under Texas's Credit Access Business (CAB) framework. The Texas Office of Consumer Credit Commissioner (OCCC) regulates CAB-registered lenders under Texas Finance Code Chapter 393.

What cash advance app gives you $100 instantly in Texas? Several apps offer up to $100 in Texas, typically within minutes for an express fee of $2.99 to $8. EarnIn, Dave, Brigit, MoneyLion, and Cleo all operate in Texas. Standard transfers (1–3 business days) are usually free; instant transfers carry a fee. Most also charge a monthly subscription ($1 to $39.99). Panda Pay's Cash Flex provides up to $100 for eligible Texas users at no additional fee beyond the standard subscription.

Does Earnin work in Texas? Yes. EarnIn operates in Texas with its standard caps: up to $150 per day and $750 per pay period. Connecticut is EarnIn's notable excluded state; Texas is not. Users must verify income through bank connection or workplace geolocation. A Maryland federal court denied EarnIn's motion to dismiss a usury class action in 2025, so the legal classification of EarnIn's product is still being litigated.

What is a Credit Access Business (CAB) in Texas? A CAB is a Texas-specific legal entity defined in Texas Finance Code Chapter 393, Subchapter G. A CAB is a broker that arranges consumer loans from a third-party lender and charges its own fee for the service. The structure lets payday and title lenders offer high-cost loans that would otherwise violate Texas's 10% usury cap because the broker fee isn't classified as interest. CABs are licensed and supervised by the Texas Office of Consumer Credit Commissioner.

Do cash advance apps require direct deposit in Texas? Most do. EarnIn, Brigit, Klover, Tilt (formerly Empower), and Cleo all require verified recurring direct deposit in a linked bank account before advancing funds. Dave and MoneyLion are more flexible. They qualify users based on overall bank transaction patterns rather than strict direct-deposit verification. Gig workers, 1099 contractors, and Texas oil-field workers with lumpy paychecks often struggle with the standard direct-deposit requirement.

The bottom line

For Texans who need under $100 to bridge a paycheck gap, the cash advance app landscape in 2026 is dense and uneven. Apps differ on amount, speed, subscription model, and — most importantly in Texas — how they fit the state's Credit Access Business framework. The comparison table earlier in this post is the shortest path to a Texas-specific answer.

Panda Pay's Cash Flex gives eligible Texas users up to $100 in cash flow support — no interest, no late fees, no credit check. Download on iOS.

Related Articles

Cash Advance Apps in Florida: How They Compare to the $10/$100 Cap

Compare cash advance apps in Florida: 2026 guide to legal options, Florida's $10-per-$100 fee cap, and non-recourse alternatives for Floridians.

These Banks Charge $0 for Overdrafts — Yours Probably Charges $35

We checked 10 banks' actual fee disclosures. Capital One, SoFi, and Ally charge $0 for overdrafts. Chase charges $34. Here's what switching saves you.

7 Places That Give You Emergency Cash Before Payday (That Aren't Payday Lenders)

Need money before payday? 7 payday loan alternatives that get you emergency cash — no 400% APR. Free resources most miss.