What Actually Happens When You Can't Pay a Bill — The Day-by-Day Timeline

When you can't pay a bill, the worst part isn't the bill itself. It's the anxiety of not knowing what happens next. Does your credit get destroyed overnight? Will they shut off your power? Are you getting evicted tomorrow?

Here's the thing most people don't realize: the consequences are completely different depending on which bill you miss. Understanding the actual timeline helps you know what to prioritize — and when to pick up the phone.

TL;DR

- Credit cards hit your credit report at day 30 — but nothing happens to your credit score before that

- Medical bills have a one-year buffer before credit reporting, and anything under $500 is never reported

- Utilities must give you written notice before shutoff (10-30 days in most states)

- Rent involves a legal process that takes 30-90 days — you're not getting evicted tomorrow

- The single best move: Call before the due date and ask about payment plans or hardship programs

Table of Contents

- Why Not All Missed Bills Are Equal

- Credit Cards: The 30-Day Clock

- Medical Bills: The Most Forgiving Timeline

- Utilities: State Rules Decide Everything

- Rent: The Legal Process Protects You

- Phone and Internet: Faster Than You'd Think

- The Real Credit Score Damage

- Your Rights When Collectors Call

- What to Do Right Now

- Frequently Asked Questions

Why Not All Missed Bills Are Equal

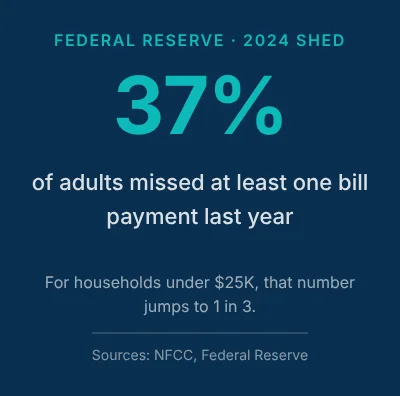

37% of adults missed at least one bill payment last year, according to the National Foundation for Credit Counseling. The Federal Reserve's 2024 household survey found that 17% of Americans can't pay all their bills on time — and for households earning under $25,000, that number jumps to 34%.

Part of the pressure is coming from non-bill costs too. Our analysis of tariff grocery costs found the average family is paying $540/year more at the grocery store than last year. Money that used to go to the electric bill is getting absorbed by food, which is why 2026 is a record year for missed payments.

If you've missed a bill, you're not alone. But the timeline of what happens next varies wildly depending on the type of bill.

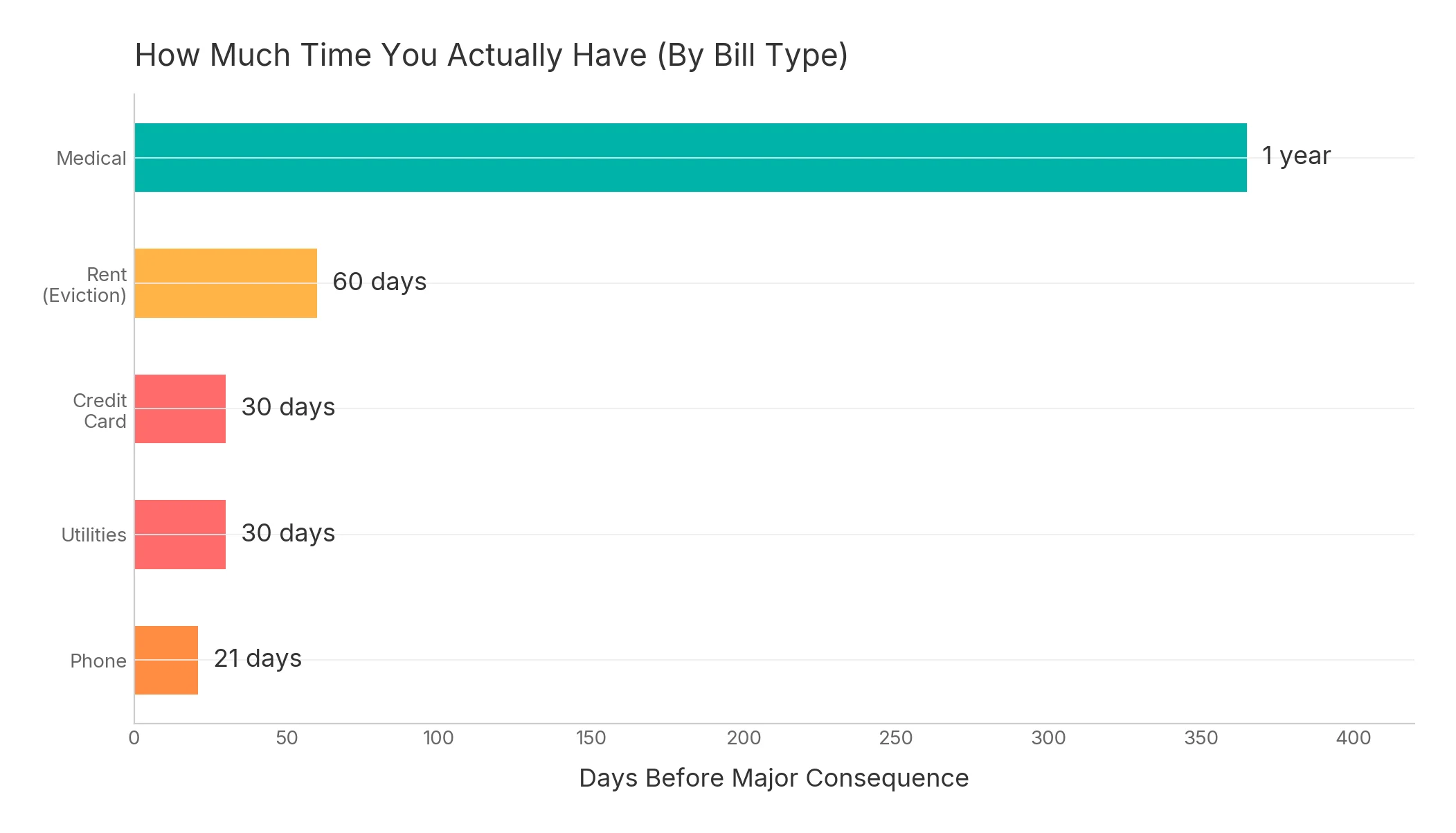

Medical debt gives you a full year before it can touch your credit report. Credit cards report at day 30. And in some states, your utilities can be disconnected just 24 hours after a final warning. Knowing which bill is which turns panic into a plan.

Credit Cards: The 30-Day Clock

Here's the exact timeline when you miss a credit card payment:

Day 1 (past due): A late fee is charged — typically $29 for a first offense, $41 for a second within six months (WalletHub 2026). Your card's penalty interest rate may also kick in, which can be as high as 29.99%. But here's what's important: nothing is reported to credit bureaus yet.

Day 30: The clock starts. Your issuer reports the missed payment to Equifax, Experian, and TransUnion as "30 days delinquent." This is where the credit score damage begins — and it's significant.

Day 60: A second delinquency mark is reported. Your score takes another hit. Some issuers may close the account entirely.

Day 90: Three straight months of non-payment. The issuer begins the charge-off process internally.

Day 120–180: The account is charged off — meaning the issuer writes it off as a loss and sells it to a collection agency. Now you owe a collector, not the original company.

The key move: Call before day 30. Most issuers will waive a first-time late fee if you ask, and they won't report the late payment if you pay before the 30-day mark. That phone call is worth protecting.

Medical Bills: The Most Forgiving Timeline

Medical debt has the longest protection timeline of any bill type — and most people don't know it.

Day 1–180: Your healthcare provider sends statements. You might get a few collection calls from the billing department. But nothing hits your credit report during this window.

After 180 days: The provider may sell your debt to a collection agency. But even then, the major credit bureaus (Equifax, Experian, and TransUnion) don't report medical collections until they're at least one year old.

If it's under $500: It will never appear on your credit report. Since 2023, the three major credit bureaus removed all medical collections under $500 from consumer reports entirely.

If you pay it: It's removed from your credit report, regardless of the amount.

The key move: Apply for the hospital's financial assistance program. Most hospitals are legally required to have one, and many will write off your entire bill if your household income is below 200–400% of the federal poverty level.

Utilities: State Rules Decide Everything

Utility shutoff timelines depend almost entirely on where you live.

Most states: Utility companies must give you 10 to 30 days of written notice before disconnecting service for non-payment (FindLaw). During that notice period, you can set up a payment plan, apply for assistance, or catch up.

Some states (Texas, Florida): Companies can disconnect with as little as 24 hours notice after posting a final warning (SavingAdvice). If you live in these states, respond to shutoff warnings immediately.

Winter protections: Many states ban utility disconnections during cold months. New York, for example, prohibits heat-related shutoffs from November 1 through April 15, and requires 30 days of notice during that period.

Medical protections: If someone in your household has a serious illness, a medical certificate from your doctor can block shutoffs for 30 days — with a one-time 30-day extension available in most states.

Credit reporting: Utilities typically only appear on your credit report if the debt is sent to collections, which usually happens 60–90 days after disconnection.

The key move: Call and ask for a hardship program or payment plan immediately. Also apply for LIHEAP (Low Income Home Energy Assistance Program) — it's a federal program that helps with utility bills, and many people who qualify never apply. If you're looking for broader options, we cover the full list of payday loan alternatives including 211, credit union PALs, community action agencies, and Salvation Army emergency assistance — any of which can help cover a utility bill before the shutoff clock runs out.

Rent: The Legal Process Protects You

If you can't pay rent, you are not getting evicted tomorrow. The legal process exists specifically to prevent that.

Day 1–5: Most leases include a 3 to 5 day grace period. No late fee yet.

Day 5–14: Late fee kicks in (amount varies by lease). Your landlord may serve you a "Pay or Quit" notice — a legal document giving you 3 to 14 days (depending on your state) to pay up or move out. (Nolo)

Day 14–30: If the notice expires and you haven't paid, your landlord can file for eviction in court. But filing doesn't mean eviction — it means a court hearing gets scheduled.

Day 30–90: Court hearing, potential judgment, appeal period, and finally a marshal or sheriff notice (typically 14 days). The full eviction process usually takes 30 to 90 days from the first missed payment.

Critical fact: You can pay the full amount owed at any point before the marshal or sheriff physically removes you — and the eviction stops.

Credit reporting: Rent is not typically reported to credit bureaus unless it's sent to collections after you move out.

The key move: Talk to your landlord before the due date. Most landlords would rather work out a payment plan than deal with the cost and hassle of eviction proceedings. A vacant unit costs them more than a late-paying tenant. If the reason you can't pay is a delayed paycheck, our borrow money until payday guide walks through the exact priority order for who to call first and how to bridge the gap without making next month worse. For state-specific guidance on emergency cash options, see our guides to cash advance apps in Texas and cash advance apps in Florida — both cover the local fee caps, which apps actually operate in-state, and non-app alternatives like 211 and state utility assistance. And if the bill stress is spilling into your relationship, our script to end money fights is a good next read.

Phone and Internet: Faster Than You'd Think

Phone and internet service can be suspended more quickly than most people expect.

Day 1–14: Late fees are applied ($5–$25 depending on your carrier). You'll get text or email reminders.

Day 21–30: Service is suspended. You can still receive calls in many cases, but can't make them. Carriers like T-Mobile typically suspend between 21 and 30 days past due.

Day 30–60: Account is cancelled. If you're financing a phone, the entire remaining device balance becomes due on your final bill immediately.

Day 60+: Sent to collections and reported to credit bureaus.

The key move: Ask about hardship programs. Every major carrier has them — they'd rather keep you as a customer on a reduced plan than lose you entirely.

The Real Credit Score Damage

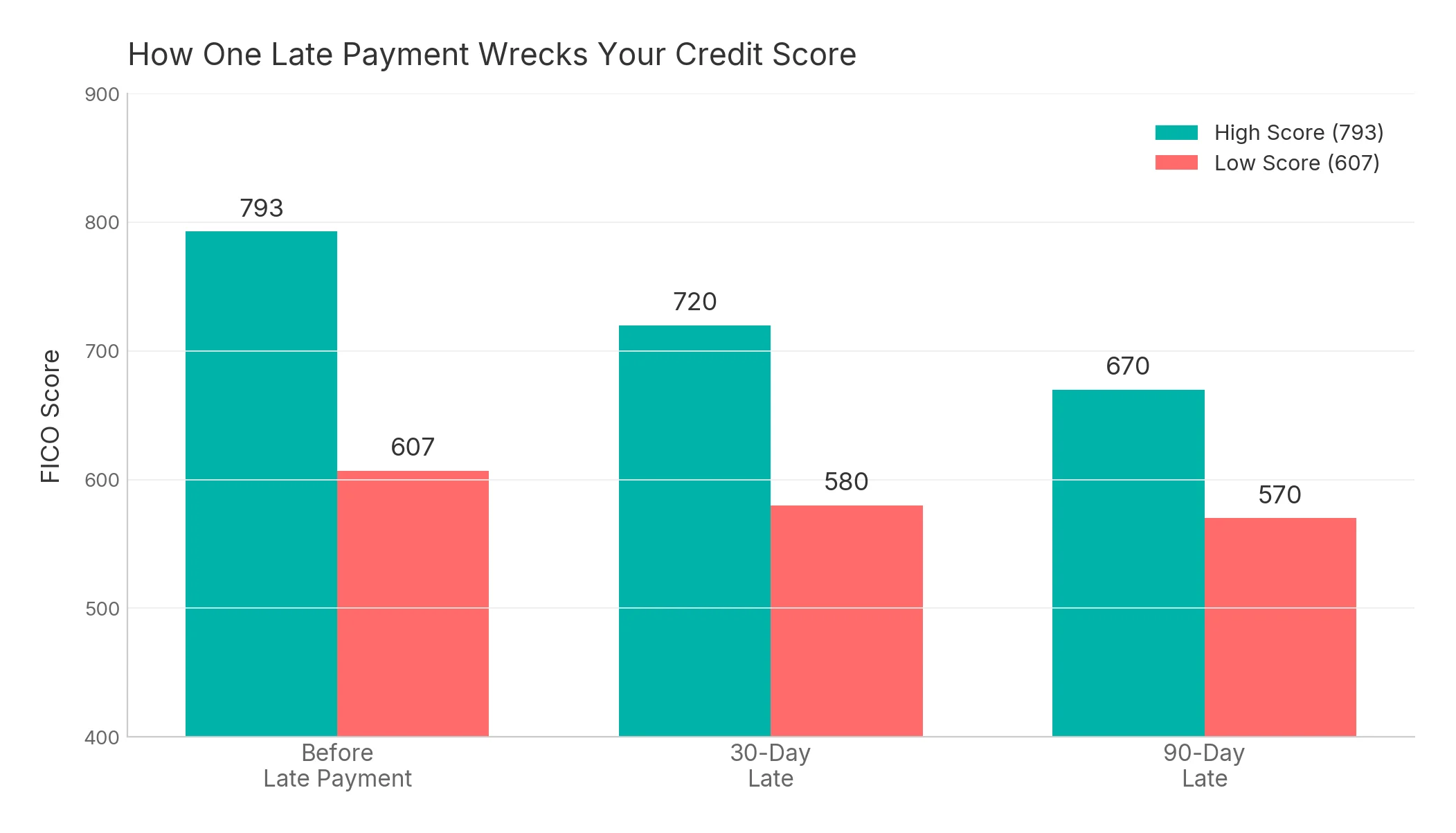

Here's what a missed payment actually does to your credit score, based on FICO's own simulations:

The pattern is counterintuitive: the higher your credit score, the more points you lose. Someone with a 793 FICO score drops to around 720 from a single 30-day late payment — a 73-point hit. Someone with a 607 drops to 580 — a smaller absolute loss, because the risk was already priced in.

A late payment stays on your credit report for 7 years from the date you missed the payment (Experian). But the impact fades over time. Most of the credit score recovery happens within the first 12–24 months, as long as you stay current.

| Scenario | Score Before | Score After | Drop |

|---|---|---|---|

| 30-day late (high credit) | 793 | 710–730 | 63–83 points |

| 90-day late (high credit) | 793 | 660–680 | 113–133 points |

| 30-day late (low credit) | 607 | 570–590 | 17–37 points |

| 90-day late (low credit) | 607 | 560–580 | 27–47 points |

Source: myFICO Score 9 simulations

What to Do Right Now

If you're reading this because you can't pay a bill right now, here's the priority order:

-

Call the company before the due date. A call before you're late is almost always more effective than silence after. Ask about hardship programs, payment plans, or extensions.

-

Prioritize by consequence. Utilities and rent affect your daily safety. Credit cards affect your credit score. Medical bills have the most flexibility. Pay what keeps your household running first.

-

Apply for assistance programs. 211.org connects you with local resources for utilities, rent, food, and more. LIHEAP covers energy bills. Hospital financial assistance programs can erase medical debt entirely.

Once you understand the timeline, you can plan. The earlier you communicate with the company, the more room there is to find a solution.

Frequently Asked Questions

How many days late before a missed payment hurts your credit score? A missed payment is reported to credit bureaus once it's 30 days past due. Before that, you'll get hit with late fees but your credit score stays untouched. After 30 days, a single late payment can drop your score by 60 to 100+ points.

Does medical debt go on your credit report? Medical debt under $500 is never reported to credit bureaus. Paid medical debt is automatically removed. Unpaid medical debt over $500 has a one-year waiting period before it can appear on your credit report, giving you time to dispute, negotiate, or set up a payment plan.

Can your utilities be shut off without warning? Most states require 10 to 30 days written notice before utilities can be disconnected. However, some states like Texas and Florida allow shutoff with as little as 24 hours notice after a final warning. Many states ban shutoffs during winter months.

How long does a late payment stay on your credit report? A late payment stays on your credit report for 7 years from the date you missed the payment. But the impact fades over time — most of the credit score recovery happens within the first 1 to 2 years if you stay current after that.

What should you do first when you can't afford a bill? Call the company before the due date. Most creditors, landlords, and utility companies have hardship programs or payment plans. A phone call before you're late is almost always more effective than silence after you've missed the payment.